April 12, 2023 10 mins

4 Ways to Achieve Success at Mid-Year Renewals

How can corporate buyers achieve optimal placement outcomes given the current reinsurance market dynamics?

Key Takeaways

-

Macroeconomic volatility has coincided with an increased frequency of extreme weather events, causing reinsurers to reassess their appetite.

-

Capital optimization is more important than ever.

-

Buyers must mitigate uncertainties with data-led portfolio differentiation.

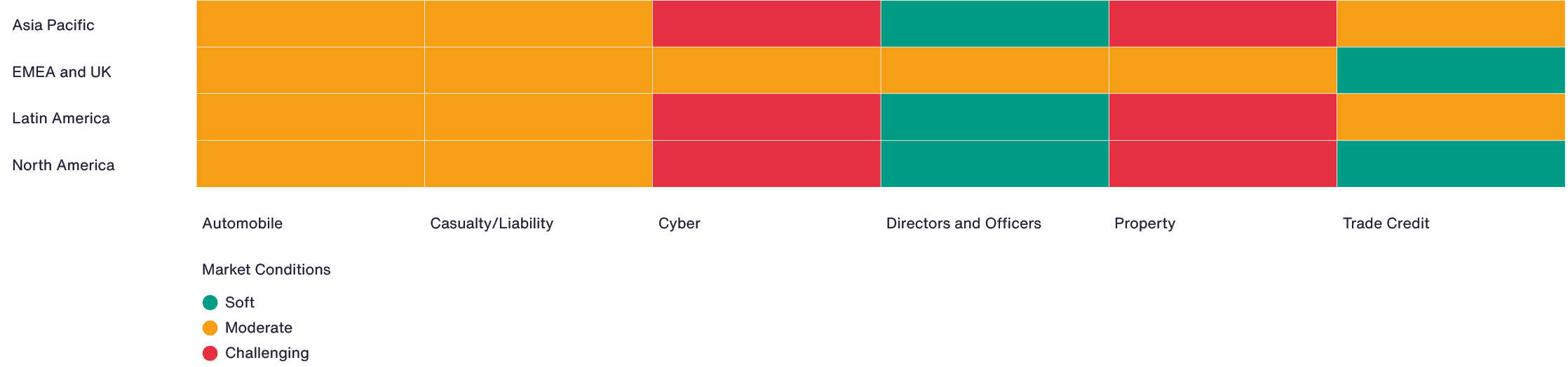

Risk managers are faced with a new reality, one that includes lower risk appetites, reduced capacity, and increased rates. Meanwhile, insurers are facing their own challenges as reinsurers have been withdrawing capacity, but high demand has meant an increase in reinsurance costs.

While ongoing inflationary pressure, supply chain challenges, geopolitical instability, and climate-driven events weigh heavily in underwriting discussions, insurers remain focused on profitable growth during mid-year reinsurance renewals.

“Competition and appetite are healthy, but insurers are closely monitoring their exposures and deploying capacity based on careful risk selection,” says Brian Wanat, Aon’s Chief Broking Officer for Commercial Risk Solutions in the US.

Trends to Watch

- Geopolitical instability, supply chain challenges and macroeconomic volatility continue to create uncertainty. Inflation and the need for increased demand for limits is still top of mind. The increase in Secondary Perils losses have also put pressure on carriers as they are not modelled for and therefore have not been priced appropriately. Losses and lack of return on equity has led to a squeeze on supply of natural catastrophe capacity.

- Demand for capacity and flexibility continues to grow, and alternatives to traditional risk transfer solutions such as captives, alternative retention and limit strategies, “buffer” programs, parametric triggers, and large limit facilities such as the Aon Client Treaty play an increasingly important role in helping risk managers execute their risk management strategies.

- A two-tiered market has developed, with products and in-appetite risks targeted for insurer growth experiencing flat or decreased pricing and abundant capacity. On the other hand, challenging, poor-performing or out-of-appetite risks are experiencing material rate increases and tight capacity, although conditions are more moderate than in previous cycles.

Industry Spotlight

Supply Chain: What is the importance of supply chain resilience amidst complexities and challenges of global supply chains?

Environmental, Social, and Governance: Having emerged as key underwriting consideration, how can you differentiate your risk?

Inflation: What alternative solutions can you look towards to manage risk as a result of inflation?

Cyber: How can you bring sustainability and scalability to your cyber claims/risk management strategies as the nature of cyber risk evolves?

Source: Aon’s latest Global Market Insights

Competition and appetite are healthy, but insurers are closely monitoring their exposures and deploying capacity based on careful risk selection.

Actions to Take

As you prepare for the mid-year renewals, you can apply the following tips:

1. Explore alternatives to help you achieve flexibility and price relief

Traditional risk transfer continues to play a vital role in achieving risk management objectives. However, in challenging markets and risk situations where capacity is limited, alternatives may provide greater flexibility and some pricing relief.

Analyze your losses and risk profile and explore which alternatives to traditional risk transfer solutions (e.g., captives, alternative retention and limit strategies, “buffer” programs, parametric triggers, and large limit facilities such as the Aon Client Treaty) may be a good fit for your risk management strategy.

Where traditional insurance is the best option, partner with capital providers who may be willing to evaluate your risk on an enterprise level, making you less susceptible to appetite contraction on your lower-performing risk types.

2. Quantify your risk to help avoid potential gaps

Asset valuation remains a top insurer priority. Remain vigilant in managing your asset valuations and coverage (sub)limits to avoid gaps. Address inflation as well as other factors such as supply chains and contractor relationships that may impact recovery and indemnity periods. Revaluate exposure to property damage and business interruption in particular.

“Insureds should remain diligent in managing values and documenting valuation methodologies to avoid gaps in coverage and limits and to secure favorable underwritinengagement,” says Luca Tassarotti, Aon’s Head of Commercial Risk Solutions for EMEA.

Clearly demonstrating how you have measured the impact of risk factors on exposures allows you to access more favorable terms and capacity. Insurer confidence in your approach will not only reduce time-consuming follow-up queries but also results in superior pricing outcomes.

3. Proactively engage with insurers to build their confidence

Even with continuous engagement with insurers throughout the year, it remains important to start renewal planning early by conducting incumbent meetings to preview appetite and pricing and analyzing data to evaluate market alternatives and explore viability.

Be forthright in providing comprehensive underwriting information – especially related to risk control and mitigation practices and actions you have taken from past recommendations – but create discussion agendas that are focused on your differentiated strengths and key concerns. Highlight lessons you have learned from past claims, and actions you are taking to build resilience.

“Also, engaging with insurers across the portfolio rather than narrowly, for one product, deepens the relationship and may encourage insurers to look beyond only in-appetite products and risks,” says Paul Young, Aon’s head of Commercial Risk Solutions for Asia.

4. Differentiate your portfolio to optimize capital efficiency

Turn challenge into opportunity by effectively using this environment to build new relationships with insurers. For instance, ESG stories and climate strategies can be a way of communicating not just what the business is doing but also has an impact on its ability to differentiate in the marketplace.

Being prepared with high quality analytics that shows what the business is doing about inflation to attack its primary exposure shifts will also be more effective at renewals than clients that rely upon reinsurers to differentiate their portfolios.

“Buyers should look to differentiate themselves not only with accurate values and data but understand carrier partnerships and how they can best manage them in 2023,” says Angela James, Aon’s Chief Broking Officer of Commercial Risk Solutions for UK.

Ultimately, providing the right information to insurers shows that you are comfortable with your risk, allowing you to manage your risk profile in today’s two-tier market.

“Whilst there are constraints in certain lines of business, the market overall is looking to grow and take the opportunity whilst it perceives the rating to be adequate,” says James. “By keeping the abovementioned lessons and tips in mind, risk managers can put themselves in a great position with insurers and maximize the desire for growth in those lines of business less challenged by the reinsurance renewals.”

To learn more about what happened at renewal for the property, casualty and specialty reinsurance markets, and a view of what it means for the future, download the full Reinsurance Market Dynamics report.

15%

or $100 billion, decline in global reinsurer capital over the year resulted in a total capital of US$575 billion at YE 2022.

Source: Aon’s latest Reinsurance Market Dynamics Report

General Disclaimer

The information contained herein and the statements expressed are of a general nature and are not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information and use sources we consider reliable, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

Terms of Use

The contents herein may not be reproduced, reused, reprinted or redistributed without the expressed written consent of Aon, unless otherwise authorized by Aon. To use information contained herein, please write to our team.

Aon's Better Being Podcast

Our Better Being podcast series, hosted by Aon Chief Wellbeing Officer Rachel Fellowes, explores wellbeing strategies and resilience. This season we cover human sustainability, kindness in the workplace, how to measure wellbeing, managing grief and more.

-

Podcast 34 mins

On Aon’s Better Being Series: The World Wellbeing Movement -

Podcast 29 mins

On Aon’s Better Being Series: Mental Health and Creating Kinder Cultures -

Podcast 28 mins

On Aon’s Better Being Series: Managing Loss and Grief -

Podcast 25 mins

On Aon’s Better Being Series: Measuring Wellbeing -

Podcast 26 mins

On Aon’s Better Being Series: Physical Wellbeing and Resilience -

Podcast 24 mins

On Aon’s Better Being Series: Human Sustainability

Cyber Labs

Stay in the loop on today's most pressing cyber security matters.

-

Cyber Labs 16 mins

Detecting “Effluence”, An Unauthenticated Confluence Web Shell -

Cyber Labs 10 mins

Financially Motivated Criminal Group Targets Telecom, Technology & Manufacturing -

Article 14 mins

From Risk to Reward: Turning Data Breaches into Deal Value -

Article 14 mins

To Combat Cyber Risk, Businesses Invest in Resilience -

Article 12 mins

For Cyber Readiness, the CISO and CRO Join Forces -

Article 19 mins

Mitigating Insider Threats: Managing Cyber Perils While Traveling Globally -

Article 38 mins

Buyer-Friendly Cyber and E&O Market: How to Take Advantage -

Article 8 mins

Managing Cyber Risk through Return on Security Investment -

Article 27 mins

Top 5 Cyber Threats To Mergers and Acquisitions -

Article 15 mins

Cyber Attacks: How to Rapidly Detect, Respond and Contain Damage -

Article 12 mins

Mitigating Insider Threats: Your Worst Cyber Threats Could be Coming from Inside

Cyber Resilience

Our Cyber Resilience collection gives you access to Aon’s latest insights on the evolving landscape of cyber threats and risk mitigation measures. Reach out to our experts to discuss how to make the right decisions to strengthen your organization’s cyber resilience.

-

Article 24 mins

Why Now is the Right Time to Customize Cyber and E&O Contracts -

Article 9 mins

8 Steps Toward Building Better Resilience Against Rising Ransomware Attacks -

Article 19 mins

Mitigating Insider Threats: Managing Cyber Perils While Traveling Globally -

Article 8 mins

Managing Cyber Risk through Return on Security Investment -

Article 12 mins

Mitigating Insider Threats: Your Worst Cyber Threats Could be Coming from Inside -

Article 17 mins

Why HR Leaders Must Help Drive Cyber Security Agenda -

Article 13 mins

Escalating Cyber Security Risks Mean Businesses Need to Build Resilience

Employee Wellbeing

Our Employee Wellbeing collection gives you access to the latest insights from Aon's human capital team. You can also reach out to the team at any time for assistance with your employee wellbeing needs.

-

Article 16 mins

How the Right Employee Wellbeing Strategy Impacts Microstress and Burnout at Work -

Article 14 mins

Making Wellbeing Part of a Company’s DNA -

Podcast 25 mins

On Aon’s Better Being Series: Measuring Wellbeing -

Article 14 mins

Addressing the Wellbeing Disconnect With a Data-Informed Strategy -

Podcast 26 mins

On Aon’s Better Being Series: Physical Wellbeing and Resilience -

Article 10 mins

Why Workforce Wellbeing is Vital to Company Performance -

Article 9 mins

COVID-19 has Permanently Changed the Way We Think About Wellbeing

Environmental, Social and Governance Insights

Explore Aon's latest environmental social and governance (ESG) insights.

-

Article 9 mins

ESG Data: How Businesses Can Use Data to Gain an Edge -

Article 12 mins

Why ESG Is Even More Important In A Crisis Like COVID-19 -

Podcast 19 mins

On Aon Podcast: Approach to DE&I in the Workplace

Q4 2023 Global Insurance Market Insights

Our Global Insurance Market Insights highlight insurance market trends across pricing, capacity, underwriting, limits, deductibles and coverages.

-

Article 20 mins

Q4 2023: Global Insurance Market Overview -

Article 19 mins

Top Risk Trends to Watch in 2024 -

Article 11 mins

Generative AI: Emerging Risks and Insurance Market Trends

Regional Results

How do the top risks on business leaders’ minds differ by region and how can these risks be mitigated? Explore the regional results to learn more.

-

Article 22 mins

Top Risks Facing Organizations in Asia Pacific -

Article 21 mins

Top Risks Facing Organizations in North America -

Article 18 mins

Top Risks Facing Organizations in Europe -

Article 19 mins

Top Risks Facing Organizations in Latin America -

Article 18 mins

Top Risks Facing Organizations in the Middle East and Africa -

Article 21 mins

Top Risks Facing Organizations in the United Kingdom

Human Capital Analytics

Our Human Capital Analytics collection gives you access to the latest insights from Aon's human capital team. Contact us to learn how Aon’s analytics capabilities helps organizations make better workforce decisions.

-

Article 19 mins

How Technology Will Transform Employee Benefits in the Next Five Years -

Podcast 20 mins

On Aon Podcast: Technology Impacting the Future of Health and Benefits -

Article 20 mins

Integrating Workforce Data to Uncover Hidden Insights -

Article 30 mins

How Employers Can Use Data to Improve Their Health Plans -

Podcast 25 mins

On Aon’s Better Being Series: Measuring Wellbeing -

Article 14 mins

Addressing the Wellbeing Disconnect With a Data-Informed Strategy -

Article 15 mins

Designing Tomorrow: Personalizing EVP, Benefits and Total Rewards -

Article 12 mins

How to Balance Cost with Growth in a Shifting Talent Market -

Article 13 mins

How Companies are Mitigating Rising Medical Costs -

Article 13 mins

How Data and Analytics Can Optimize HR Programs

Insights for HR

Explore our hand-picked insights for human resources professionals.

-

Article 9 mins

COVID-19 has Permanently Changed the Way We Think About Wellbeing -

Article 11 mins

DE&I in Benefits Plans: A Global Perspective -

Article 13 mins

How Data and Analytics Can Optimize HR Programs -

Article 17 mins

Why HR Leaders Must Help Drive Cyber Security Agenda -

Article 10 mins

Case Study: The LPGA Unlocks Talent Potential with Data -

Article 16 mins

Navigating the New EU Directive on Pay Transparency -

Article 14 mins

How to Design Better Talent Assessment to Promote DE&I -

Article 8 mins

Training and Transforming Managers for the Future of Work -

Article 10 mins

Rethinking Your Total Rewards Programs During Mergers and Acquisitions -

Article 21 mins

Building a Resilient Workforce That Steers Organizational Success | An Outlook Across Industries

Workforce

Our Workforce Collection provides access to the latest insights from Aon’s Human Capital team on topics ranging from health and benefits, retirement and talent practices. You can reach out to our team at any time to learn how we can help address emerging workforce challenges.

-

Article 16 mins

Driving Inclusion and Diversity with Employee Benefits -

Article 24 mins

Five Big Human Resources Trends to Watch in 2024 -

Article 13 mins

How Companies are Mitigating Rising Medical Costs -

Report 2 mins

The Global Medical Trend Rates Report 2024 -

Podcast 26 mins

On Aon’s Better Being Series: Physical Wellbeing and Resilience -

Article 16 mins

How the Right Employee Wellbeing Strategy Impacts Microstress and Burnout at Work -

Article 14 mins

Addressing the Wellbeing Disconnect With a Data-Informed Strategy -

Article 28 mins

Advancing Women’s Health and Equity Through Benefits and Support -

Podcast 20 mins

On Aon Podcast: Technology Impacting the Future of Health and Benefits -

Article 12 mins

How Collective Retirement Plans Help Support Financial Sustainability -

Article 15 mins

Four Ways Retirement Plans Can Reduce the Gender Savings Gap -

Article 24 mins

Understanding and Preparing for the Rise in Pay Transparency

Mergers and Acquisitions

Our Mergers and Acquisitions (M&A) collection gives you access to the latest insights from Aon's thought leaders to help dealmakers make better decisions. Explore our latest insights and reach out to the team at any time for assistance with transaction challenges and opportunities.

-

Article 21 mins

Exit Strategy Value Creation Opportunities Exist as Economic Pressures Persist -

Article 10 mins

Future Trends for Financial Sponsors: Secondary Transactions -

Article 16 mins

ESG Factors are Carrying Increasing Importance in Mergers and Acquisitions Dealmaking -

Article 24 mins

3 Ways to Unlock M&A Value in a Challenging Credit Environment -

Article 14 mins

An Ever-Complex Global Tax Environment Requires Strong M&A Risk Solutions -

Article 8 mins

Project Management for HR: The Secret Behind a Successful M&A Deal -

Article 18 mins

Cultural Alignment Planning Drives M&A Success -

Article 14 mins

From Risk to Reward: Turning Data Breaches into Deal Value

Navigating Volatility

How do businesses navigate their way through new forms of volatility and make decisions that protect and grow their organizations?

Parametric Insurance

Our Parametric Insurance Collection provides ways your organization can benefit from this simple, straightforward and fast-paying risk transfer solution. Reach out to learn how we can help you make better decisions to manage your catastrophe exposures and near-term volatility.

-

Article 21 mins

Why Parametric Solutions Should Be Part of Your Next Renewal Conversation -

Article 13 mins

Parametric Insurance: A Complement to Traditional Property Coverage -

Article 14 mins

Using Parametric Insurance to Match Capital to Climate Risk -

Article 10 mins

Using Parametric Insurance to Close the Earthquake Protection Gap -

Article 21 mins

How Technology Enhancements are Boosting Parametric

Property Risk Management

Our Property Risk Management collection gives you access to the latest insights from Aon's thought leaders to help organizations make better decisions. Explore our latest insights to learn how your organization can benefit from property risk management.

-

Article 18 mins

Navigating the Challenges of the Year-End Property Market -

Article 10 mins

Four Steps to Develop Strong Property Risk Coverage in a Hardening Market -

Podcast 19 mins

On Aon Podcast: Navigating and Preparing for Catastrophes -

Article 13 mins

Parametric Insurance: A Complement to Traditional Property Coverage -

Article 12 mins

Navigating Climate Risk Using Multiple Models and Data Sets -

Article 9 mins

Rising Losses From Severe Convection Storms Mostly Explained by Exposure Growth -

Article 21 mins

Why Parametric Solutions Should Be Part of Your Next Renewal Conversation -

Article 10 mins

Using Parametric Insurance to Close the Earthquake Protection Gap

Technology

Our Technology Collection provides access to the latest insights from Aon's thought leaders on navigating the evolving risks and opportunities of technology. Reach out to the team to learn how we can help you use technology to make better decisions for the future.

-

Article 20 mins

5 Ways Artificial Intelligence can Boost Claims Management -

Article 8 mins

Artificial Intelligence and the Next Frontier for Financial Institutions -

Article 12 mins

Mitigating Insider Threats: Your Worst Cyber Threats Could be Coming from Inside -

Article 9 mins

8 Steps Toward Building Better Resilience Against Rising Ransomware Attacks -

Article 18 mins

Overcoming the Reputational Cost of Cyber Attacks: The 10-Day Plan -

Article 17 mins

Why HR Leaders Must Help Drive Cyber Security Agenda -

Article 15 mins

How to Futureproof Data and Analytics Capabilities for Reinsurers

Top 10 Global Risks

Trade, technology, weather and workforce stability are the central forces in today’s risk landscape.

-

Article 14 mins

Cyber Attack or Data Breach -

Article 9 mins

Business Interruption -

Article 10 mins

Economic Slowdown or Slow Recovery -

Article 12 mins

Failure to Attract or Retain Top Talent -

Article 12 mins

Regulatory or Legislative Changes -

Article 10 mins

Supply Chain or Distribution Failure -

Article 14 mins

Commodity Price Risk or Scarcity of Materials -

Article 10 mins

Damage to Brand or Reputation -

Article 10 mins

Failure to Innovate or Meet Customer Needs -

Article 10 mins

Increasing Competition

Trade

Our Trade Collection gives you access to the latest insights from Aon's thought leaders on navigating the evolving risks and opportunities for international business. Reach out to our team to understand how to make better decisions around macro trends and why they matter to businesses.

-

Report 5 mins

Global Risk Management Survey -

Article 10 mins

Four Steps to Develop Strong Property Risk Coverage in a Hardening Market -

Article 10 mins

Managing Project Risks: 5 Ways Credit Solutions Can Help -

Article 34 mins

Cutting Supply Chains: How to Achieve More Reward with Less Risk -

Article 24 mins

Driving Private Equity Value Creation Through Credit Solutions -

Article 12 mins

Tips for 2024 Salary Increase Planning -

Article 12 mins

4 Steps to Help Take Advantage of a Buyer-Friendly Directors' & Officers' Market -

Article 18 mins

Managing Reputational Risks in Global Supply Chains -

Article 10 mins

How an Outsourced Chief Investment Officer Can Help Improve Governance and Manage Complexity -

Article 12 mins

Decarbonizing Your Business: Finding the Right Insurance and Strategy -

Article 17 mins

Reputation Analytics as a Leading Indicator of ESG Risk

Weather

With a changing climate, organizations in all sectors will need to protect their people and physical assets, reduce their carbon footprint, and invest in new solutions to thrive. Our Weather Collection provides you with critical insights to be prepared.

-

Report 5 mins

Climate and Catastrophe Insight -

Article 26 mins

How Investors are Making Better Decisions Amid a Changing Climate -

Article 12 mins

Improving Agricultural Practices to Address Climate Risks -

Article 22 mins

Understanding Freeze Risk in a Changing Climate -

Article 19 mins

Insurance Plays a Key Role in Transitioning to a Low Carbon Future -

Article 17 mins

How Academic Research Can Help Drive Climate Risk Resilience -

Podcast 11 mins

On Aon Podcast: Climate Science Through Academic Collaboration -

Article 11 mins

How Companies Are Using Climate Modeling to Improve Risk Decisions -

Podcast 9 mins

On Aon Insights: Climate and Supply Chain -

Article 14 mins

Using Parametric Insurance to Match Capital to Climate Risk -

Article 27 mins

How the Construction Industry is Navigating Climate Change -

Article 16 mins

Record Heatwaves: Protecting Employee Health and Safety

Workforce Resilience

Our Workforce Resilience collection gives you access to the latest insights from Aon's Human Capital team. You can reach out to the team at any time for questions about how we can assess gaps and help build a more resilience workforce.

-

Article 12 mins

Using Data to Close Workforce Gaps in Financial Institutions -

Article 11 mins

Using Data to Close Workforce Gaps in Retail Companies -

Article 15 mins

Using Data to Close Workforce Gaps in Technology Companies -

Article 8 mins

Using Data to Close Workforce Gaps in Manufacturing Companies -

Article 14 mins

Using Data to Close Workforce Gaps in Life Sciences Companies -

Report 9 mins

Measure Workforce Resilience for Better Business Outcomes -

Podcast 21 mins

On Aon Podcast: Methodology to Predict Employee Performance for the LPGA -

Article 17 mins

What Does a Resilient Workforce Look Like? -

Article 8 mins

Training and Transforming Managers for the Future of Work -

Article 21 mins

Building a Resilient Workforce That Steers Organizational Success | An Outlook Across Industries

More Like This

-

Article 24 mins

Capturing Carbon on the Critical Pathway to Net Zero

As the world races to reduce climate risks and limit CO<sub>2</sub> emissions, the demand for scalable and cost-effective decarbonization technologies is increasing. Carbon capture projects form an important part of the low carbon energy transition, bringing both challenges and opportunities.

-

Article 13 mins

Protecting North American Contractors from Extreme Heat Risks with Parametric

Growing extreme heat conditions have escalated risks, delays and costs for the construction industry in North America. Parametric insurance can help protect against such risks, offering contractors and building owners agility, efficiency and flexibility.

-

Article 21 mins

How Insurance Can Help Hedge Potential Exposures Under the New Unified Patent Court System

The launch of the Unified Patent Court allows for a new patent filing process across Europe using a centralized system. While this brings significant financial and operational benefits, navigating these changes will demand a robust litigation risk management strategy.