Impact on Sales Processes

The highly competitive nature of the current

M&A market has forced buyers to adjust or even

transform the way they approach the deal

process. One area of focus in particular has

emerged for buyers as a crucial factor in winning

deals: improving their ability to close quickly. In

our survey of M&A dealmakers, a plurality of

respondents identified this as the top strategy

they have employed over the last 12-24 months

in response to greater competition for targets.

They also said the main factor that derails a

buy-side deal in the current market is a

competing bid being made with better speed or

certainty to close.

“The M&A market has changed significantly over

the last decade, and we don’t have the same

amount of time to make decisions as we used

to,” said a managing director at a US-based

private equity firm. “The competition is so

intense that any delay in closing a deal can cause

you to lose out to a competitor. We have

become more selective in our targeting to make

sure we have the confidence to close a deal

quickly.”

In this fast-moving environment, R&W insurance

is a tool that can alleviate elongated negotiation

around the scope of representations and

warranties and indemnification, helping the two

parties to close a deal more quickly. Indeed,

R&W insurance often features prominently in the

current deal process because of these benefits,

increasingly becoming the “standard” approach,

with its utilization the cost of admission for many

sales processes.

M&A insurance solutions can also provide an

alternative to competing on price – another key

issue as buyers seek to outbid each other for a

shrinking pool of attractive targets. Our survey

respondents identified “adjusting return

expectations” as another core strategy to

manage the degree of competition on the M&A

market, suggesting some discipline around their

approach to valuations, and PE and corporate

respondents also said “outbidding competing

buyers without overpaying” would be a key

hurdle they expect to face in 2019.

“We’ve implemented a disciplined deal-making

process so that we can compete aggressively in

the highly competitive M&A market while

coping with high valuations,” said a senior

director for corporate development at a

US-based company. “It’s all about how the deal

will create value for our company and how far

we can go with valuations so that we can close

the deal and at the same time the valuations

remain viable.”

Acquirers will need every tool at their disposal to

prevent valuations from rising even higher than

the current rates. In 2018, the median sale

multiple for strategic deals in North America

reached 11.2x EBITDA, while for private equity

buyouts the median multiple rose to 12.7x

EBITDA, according to Mergermarket data. M&A

insurance policies can be one helpful tool

toward this end, allowing PE and corporate

buyers alike to minimize or eliminate escrow and

maximize sellers’ cash at closing.

Impact on Deal Structure

With sellers wielding significant leverage in many

transactions, the number of deals structured with

no seller indemnity is on the rise. Based on Aon’s

results in 2018, 75% of deals included some form of

seller indemnity and 25% were negotiated with no

seller indemnity, also known as a “public-style

deal,” with R&W insurance as the sole recourse –

indicating a slight shift toward no-seller-indemnity

structures compared to 2017. The consistent

utilization of the o-seller-indemnity structure

underscores two important aspects of the current

M&A market: first, the continued briskness of sales

processes in which sellers can demand very

favorable deal terms, including the elimination of

post-closing indemnification for breaches of reps

and warranties; and second, buyers’ comfort with

insurance as a replacement for a traditional seller

indemnity or escrow.

Looking at deal sizes for each type of structure, the

median enterprise value for transactions completed

with limited seller indemnity was $100M, compared

to a median of $333M for those structured with no

seller indemnity. The average policy retention for

limited-seller-indemnity deals was 1.23%, versus

1.00% for no-seller-indemnity deals, signaling

greater pressure for reduced retentions when borne

exclusively by the buyer under the

no-seller-indemnity structure. The tendency for

no-seller-indemnity structures to be used on larger

deals contributes to the lower average retention, as

market conditions have allowed for sub-1%

retentions on deal sizes of $500M or more, with

some markets showing flexibility for sub-1%

retentions below this threshold as well.

Industry Insights

As R&W insurance further penetrates the North American M&A market and insurers continue to increase

their appetite for deals, insurance played a role in more transactions in challenging industries in 2018.

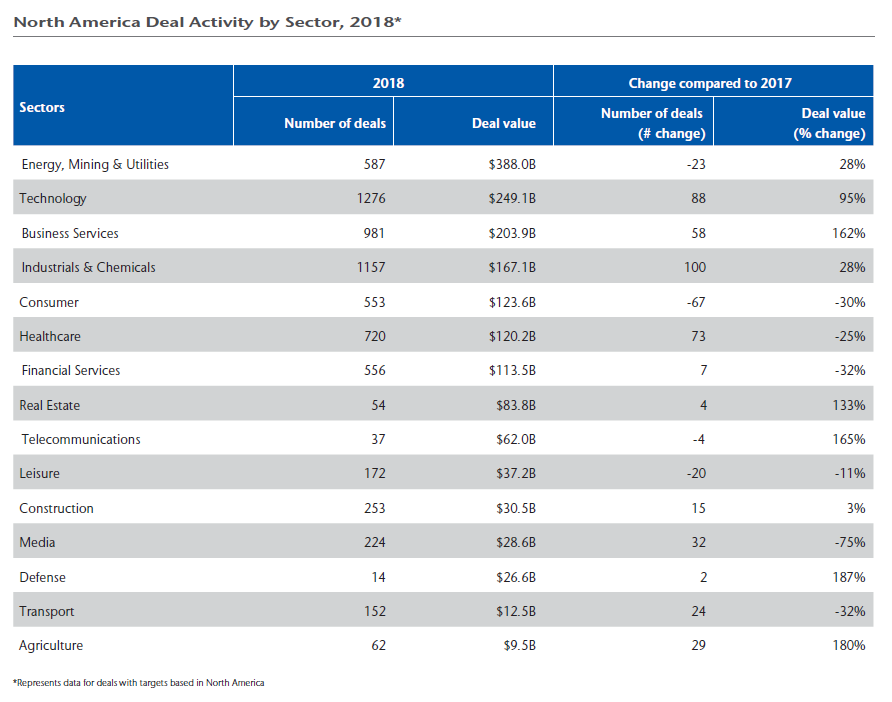

M&A activity grew in most sectors last year, with energy, mining & utilities and technology holding the

top two positions by deal value. The vast majority of sectors saw increases in the number of deals –

industrials & chemicals and healthcare in particular saw substantial growth in transaction volume.

Regardless of sector, buyers are increasingly seeking targets with attractive technology assets, as the

demand for digital tools on the part of consumers and suppliers alike grows rapidly. As a result, sub-sectors

such as fintech, digital health, e-commerce, robotics, and software are expected to attract significant buyer

attention in the year ahead.

Healthcare

Fifty-nine deals were announced in the healthcare space that included transaction insurance in 2018,

representing over $2 billion of insurance limits with more than 10 insurers active in this space, according to

Aon data. Target businesses included optometrists, veterinary practices, surgical and medical device

companies, acute care medical centers, as well as substance abuse and addiction treatment facilities.

Deal activity in the healthcare sector expanded by volume in 2018, increasing to a total of 720 transactions

valued at $120.2B. At the top end of the market, pharmaceutical companies and large insurers drove

mega-deal activity, as the largest healthcare players transform themselves to adapt to changing market

conditions. Private equity has been extremely active across deal sizes and especially in the middle market,

making acquisitions to add to platform companies and consolidating individual medical practices. There

were 194 PE deals for healthcare targets in North America in 2018, an increase of 28 compared to the

previous year, with total transaction value of $26.9B.

Financial Institutions & Insurance Companies

Ten deals for targets in the financial institutions & insurance space were announced last year with

transaction insurance, representing nearly $250M in insurance limits. Historically, this sector has met with

tepid to no market appetite from insurers, with just a handful of insurers considering such deals.

Target companies insured in these deals involved insurance agencies, life insurance, supplemental health

and annuity platforms, workers’ compensation insurers, capital management firms and specialty finance

companies. Buyers should be prepared for increased underwriting focus on regulatory compliance matters

and cyber/data privacy, with exclusions common around adequacy of reserves and veracity of

underwriting files.

Financial services M&A volume increased modestly in 2018, with a total of 556 deals valued at an

aggregate $113.5B. In addition to a substantial number of insurance company transactions, targets

attracting strong buyer interest include those in sub-sectors such as payments technology, B2B software,

and digital tools for wealth management and capital markets.

Energy

In 2018, several acquisitions of wind and solar developers utilized R&W insurance, including one deal

requiring a hybrid tax and R&W insurance policy to insure both the loss of tax credits (including recapture

due to future events) as well as the full suite of reps and warranties given by an uncreditworthy solar

developer to a large bank. A total of $1.6B in tax insurance limits were placed across 58 transactions,

insuring a number of risks associated with tax equity investments in the energy space, such as the

investment structure not being respected, the transaction not qualifying for projected tax benefits, and the

loss of tax benefits through recapture.

Over 40 deals in the energy space, including oil and gas and power transactions, utilized R&W insurance in

2018, representing $2.6B in limits placed. In particular, we observed an increased use of insurance across

infrastructure deals as well as along the vertical chain (upstream, midstream, downstream). R&W

insurance has also developed to respond to unique risks relevant to upstream oil and gas transactions,

insuring traditional representations as well as special warranty of title matters to provide buyers with

post-closing protection for title defects that arose by, through or under the seller.

Intellectual Property (IP)

Over the past decade, there has been a major shift away from tangible assets to intangible assets. Today,

approximately $19 trillion in market value, or nearly 85% of the value of the S&P 500, is represented by

intangible assets, and investment in intellectual property has changed the global landscape across

industries and regions. Many companies, however, have been slow to adopt new approaches to

managing, assessing and creating value around their intellectual property portfolios in a manner that fully

captures its value potential. Across the deal lifecycle, the implications for M&A professionals is significant as

they look to maximize returns on their investments while managing associated risks.

Intellectual property has implications for both sides of the deal. For buyers, valuing the property accurately

and understanding its relative value against competing property in the market is critical to setting the right

price. For sellers, the hold period provides an opportunity to grow enterprise value by taking a strategic

approach to managing, pruning and developing the intellectual property, and to articulate that growth

effectively to Wall Street at the time of sale.

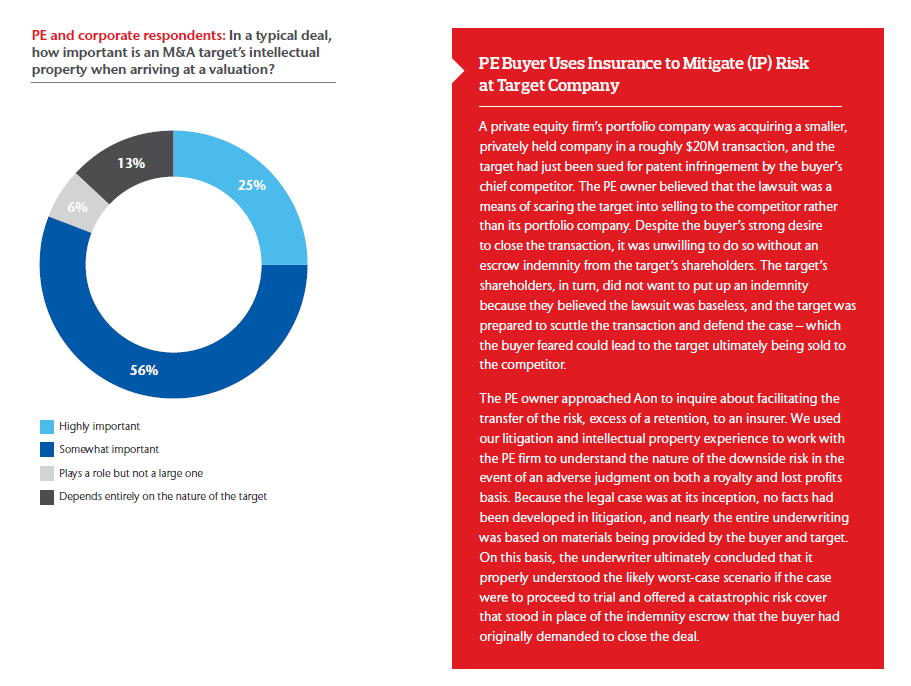

In our survey of M&A professionals, 81% of respondents said that a target’s IP has become important in

arriving at a valuation, with 25% saying it is “highly important.” “IP has emerged as a critical component of

deal-making, and many companies are investing heavily to secure attractive and promising technology and

products,” said an M&A partner at a Canadian law firm. “The problem with IP is that it loses its value and

significance at the same pace as it gained value. Unless the IP is very promising and sustains its value over

the long term, paying top dollar for it can be risky.”