Closing the Protection Gap

Click here to view the printable version

Every year catastrophes wreak havoc on people in every corner of the globe, and the consequences are getting worse. The frequency of natural disasters is increasing, and the damage they cause will be greater as the world population becomes more urban and concentrated in areas prone to catastrophe. In 2017, five wildfires made the top 20 list of the most destructive in California’s history. Hurricane Harvey resulted in 60 inches of rain inundating Houston, TX, easily beating the prior record set in 1978. Puerto Rican officials can finally claim that power has been restored to 100 percent of its residents nearly one year after Hurricane Maria devastated the island. Flooding in China, an earthquake in Mexico, and an extreme drought in southern Europe all add up to $368 billion in economic losses; the second-highest year for natural disasters globally.

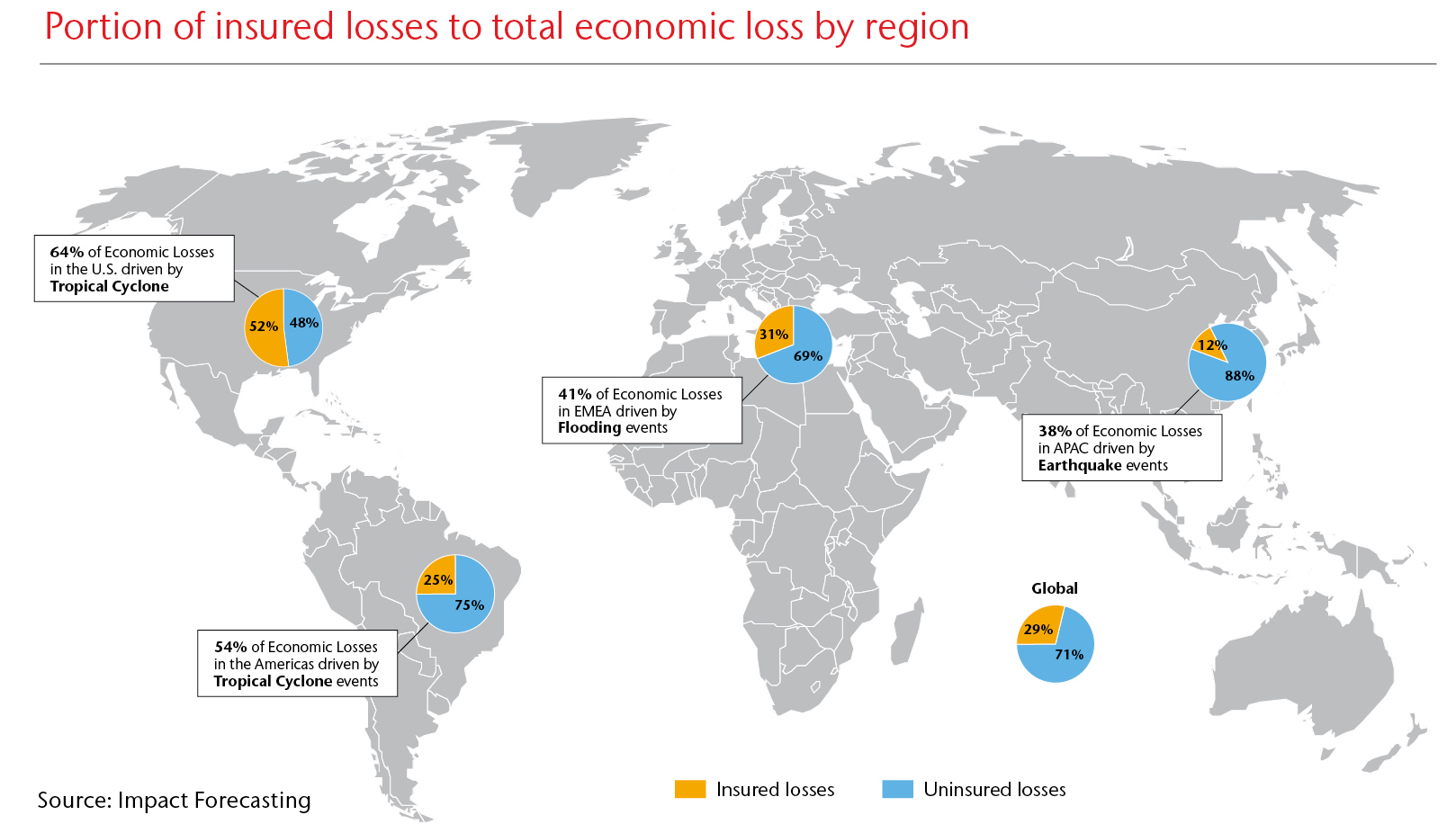

Insurance is an essential part of a community’s resilience, but last year the insurance industry covered less than 40 percent of the losses, leading to a global insurance protection gap of $231 billion. The protection gap is the difference between the economic loss of a catastrophe and the amount that is covered by insurance, and it can include clean-up costs, uninsured property damage, damaged infrastructure, emergency relief, and foregone revenues. Government programs can fill the gap in developed regions, but increasingly, these costs are being borne by the most poor and vulnerable members of our society. According to the World Bank, the destruction caused by extreme weather pushes 26 million people into poverty each year and has a direct impact on the long-term economic recovery of a region affected by catastrophe. In the absence of sufficient insurance coverage, the impact on economic growth can be not only detrimental in the short-term, but permanent.

Insurance is an essential part of a community’s resilience, but last year the insurance industry covered less than 40 percent of the losses, leading to a global insurance protection gap of $231 billion. The protection gap is the difference between the economic loss of a catastrophe and the amount that is covered by insurance, and it can include clean-up costs, uninsured property damage, damaged infrastructure, emergency relief, and foregone revenues. Government programs can fill the gap in developed regions, but increasingly, these costs are being borne by the most poor and vulnerable members of our society. According to the World Bank, the destruction caused by extreme weather pushes 26 million people into poverty each year and has a direct impact on the long-term economic recovery of a region affected by catastrophe. In the absence of sufficient insurance coverage, the impact on economic growth can be not only detrimental in the short-term, but permanent.

Governments, businesses, and individuals alike play a role in closing the protection gap, ensuring that communities can rebuild quickly and efficiently after disaster strikes. Insurance is an important partner. Fundamentally, building resilience is supported by having speedy and reliable financial relief funneled to those who need it most after an event occurs. Additionally, providing incentives that reduce risky behavior and promote risk mitigation efforts are all benefits that a robust insurance market can provide. This article will review what goes into the protection gap and its root causes, and will provide examples of innovative ways the insurance industry is stepping up to close the gap.

Root causes of the protection gap

Education, awareness, and cultural limitations are the most frequently cited causes for the protection gap; indeed, in many parts of the world, cultural tendencies lean more towards increasing personal savings over purchasing insurance. The gap is also exacerbated by immature and ineffective regulatory frameworks, which lead to mismanagement, corporate defaults, and scams, showing deep distrust of the industry in many developing economies. Lack of compulsory insurance requirements, combined with a tendency to underestimate the real cost of risk, reinforces the decision not to utilize insurance.

Eighty-five percent of the losses from the 2011 Tohoku earthquake and tsunami in Japan were borne by the communities and businesses impacted by the event. This protection gap was driven mostly by underinsurance in commercial lines. Rather than buy insurance, Japanese companies have a greater tendency to self-prepare by investing in more resilient infrastructure and developing sophisticated business continuity plans. Insurance prices offered by the international reinsurance market are sometimes judged to be too expensive by Japanese businesses.

Government-funded disaster relief programs can also reduce the incentive for individuals to purchase insurance. For instance, Hurricane Harvey had a 70 percent protection gap due to the large amount of flooding caused by the storm, and only 15 percent of those affected by the storm had some form of flood insurance. In the U.S., the absence of risk-driven pricing leads to a lack of awareness of the true cost of the risk, and when combined with a belief that individuals will be “bailed-out” after the next storm, this removes any motivation for consumers to purchase adequate coverage.

The insurance industry has been innovating to solve this problem for years, and with increasing pressure from governmental organizations to increase resilience, the opportunity for the industry to drive solutions has never been better. The Insurance Development Forum (IDF) was launched in 2016 explicitly as an answer to the resiliency challenges laid out in various global agreements, such as the Paris Agreement and the U.N. Sendai Framework for Disaster Risk Reduction 2015-2030. The IDF states that a “1 percent increase in insurance penetration can reduce the disaster recovery burden on taxpayers by 22 percent”.

The insurance industry has been innovating to solve this problem for years, and with increasing pressure from governmental organizations to increase resilience, the opportunity for the industry to drive solutions has never been better. The Insurance Development Forum (IDF) was launched in 2016 explicitly as an answer to the resiliency challenges laid out in various global agreements, such as the Paris Agreement and the U.N. Sendai Framework for Disaster Risk Reduction 2015-2030. The IDF states that a “1 percent increase in insurance penetration can reduce the disaster recovery burden on taxpayers by 22 percent”.

The role of insurance penetration

While geographic vulnerability to natural disasters provides a good indication of how a nation’s economy will be affected following a catastrophic event, it is also crucial to account for the role that insurance penetration has in expediting the journey back to growth. The immediate destruction after an event causes a wide array of negative social and economic impacts, but can also serve as a boon to GDP growth as money flows in to begin reconstruction efforts. Insurance payouts not only play a role in stimulating that growth, but can also help to reduce the negative impact to GDP caused by the loss of productive capacity due to risk reduction incentives that insurance provides before the event occurs.

Annual GDP growth rates may see a short-term boon after an event due to an influx of insurance payments, external aid, and reconstruction spending. Studies show that the cumulative loss in regions with insufficient insurance recoveries can be volumes larger than the short-term impact on GDP. The Bank for International Settlements studied the relationship between long-run economic growth and insurance penetration and found that “a typical catastrophe causes a drop in growth of 0.6 to 1.0 percent on impact, and results in a cumulative output loss of two to three times this magnitude”.

Annual GDP growth rates may see a short-term boon after an event due to an influx of insurance payments, external aid, and reconstruction spending. Studies show that the cumulative loss in regions with insufficient insurance recoveries can be volumes larger than the short-term impact on GDP. The Bank for International Settlements studied the relationship between long-run economic growth and insurance penetration and found that “a typical catastrophe causes a drop in growth of 0.6 to 1.0 percent on impact, and results in a cumulative output loss of two to three times this magnitude”.

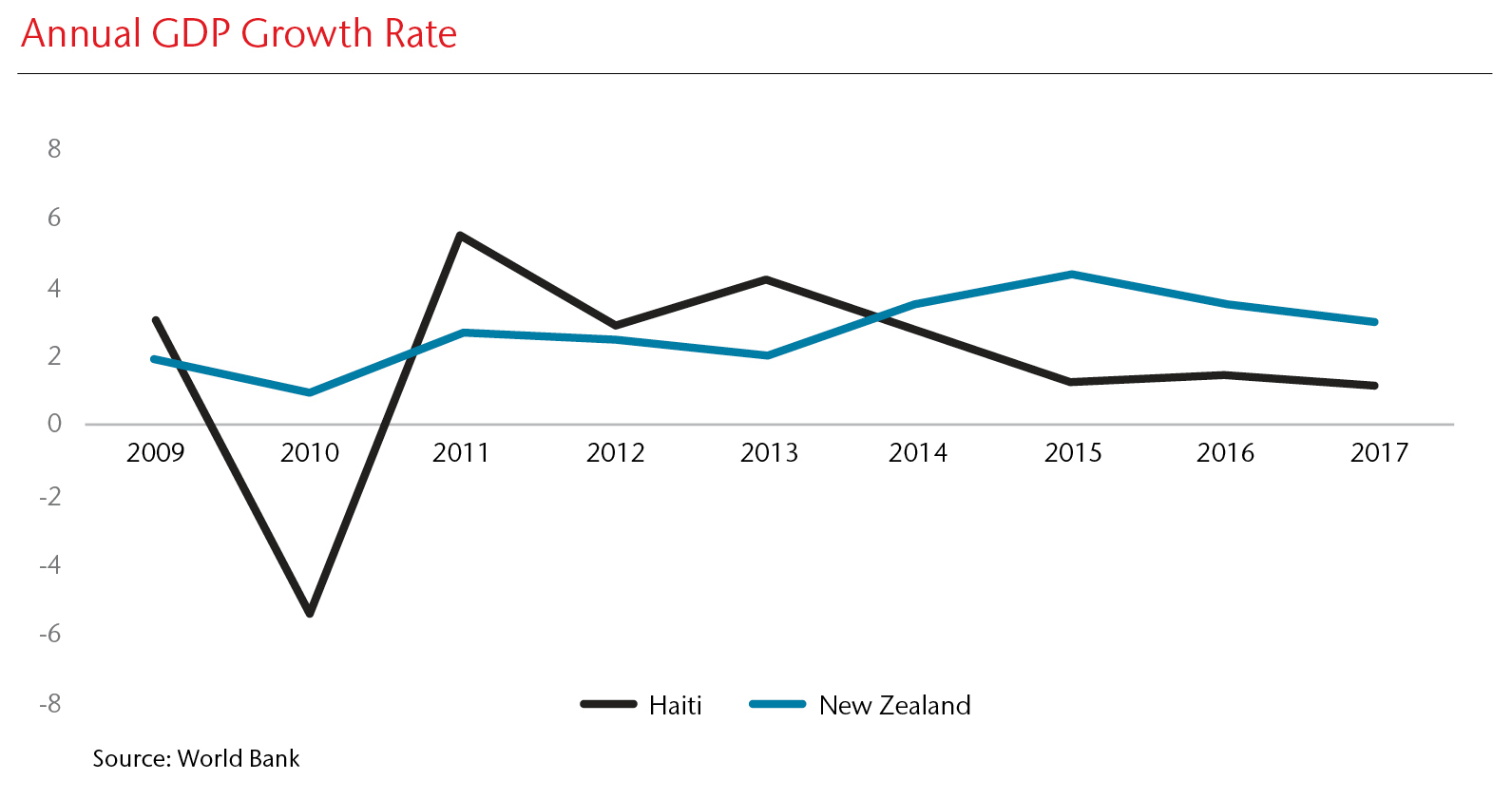

Case study: New Zealand versus Haiti earthquakes - eight years later

A case in point is provided by comparing New Zealand and Haiti. Both are earthquake-prone island nations that were struck with large earthquakes in 2010 and 2011, but the recovery of both nations has contrasted starkly, in part because of the difference in insurance penetration. The sizable difference in overall economic standing must be considered when comparing the recovery of both nations. However, this does not diminish the impact that insurance has had on long-run growth in both nations.

In Haiti, the 2010 earthquake resulted in $8 billion of economic loss (126 percent of GDP), of which only 1 percent was covered by insurance. 220,000 people lost their lives in the event, 40 percent of the population was dislocated, and GDP growth dropped from 3.5 percent to a negative 5.5 percent in 2010. The most distressing component in Haiti’s recovery has been the devastating outbreak of cholera, which is estimated to have killed 9,480 Haitians to date. Reports vary, but some estimates place 80,000 people still living in non-permanent structures while unemployment sits at 40 percent.

The New Zealand earthquake in 2011, by contrast, caused an estimated $26 billion in economic loss of which more than 50 percent was insured. Immediately after the event, New Zealand was able to maintain positive growth in 2011, driven primarily by an increased volume of funds being funneled to those needing it most, bolstering economic activity. It is important to consider that New Zealand has a more complex insurance market due to the Earthquake Commission, a government-provided insurance product for residential risks. The EQC has come under intense criticism due to slower response times than private insurers. By mid-2014, however, more than 90 percent of all claims had been finalized. While progress has been admittedly slow, the resiliency of Christchurch residents is evident.

Public-private partnerships

Boosting public-private partnerships can close the protection gap by focusing insurance industry efforts on governments rather than consumers, who may be harder to reach. The industry can partner with governments and nonprofit entities to enhance regulation and provide protection to taxpayers, by lowering the potential financial burden on a government following a disaster. For example, the U.S. Congress created the National Flood Insurance Program (NFIP) in 1968 to provide homeowners with affordable flood insurance when the private market deemed flood an “uninsurable” peril. After Hurricanes Katrina (2015) and Sandy (2008), the NFIP became indebted to the  U.S. Treasury to the tune of $23 billion, prompting the NFIP to purchase $1 billion of reinsurance to transfer the risk. The agreement was in place in time to fully protect the NFIP for losses from Hurricanes Harvey and Irma in 2017, saving taxpayers approximately $850 million. In addition to de-risking government balance sheets, insurers can also increase penetration by participating in risk-pooling opportunities through partnership with developmental entities, for example, the historic $1.36 billion in earthquake protection provided to Chile, Colombia, Mexico, and Peru by the World Bank.

U.S. Treasury to the tune of $23 billion, prompting the NFIP to purchase $1 billion of reinsurance to transfer the risk. The agreement was in place in time to fully protect the NFIP for losses from Hurricanes Harvey and Irma in 2017, saving taxpayers approximately $850 million. In addition to de-risking government balance sheets, insurers can also increase penetration by participating in risk-pooling opportunities through partnership with developmental entities, for example, the historic $1.36 billion in earthquake protection provided to Chile, Colombia, Mexico, and Peru by the World Bank.

Case study: Caribbean Catastrophe Risk Insurance Facility builds resilience by pooling risk

On a global scale, intergovernmental organizations have also played a crucial role in pursuing risk-mitigation schemes, such as the Caribbean Catastrophe Risk Insurance Facility or CCRIF, the world’s first multi-country risk pooling scheme. Prompted by Hurricane Ivan in 2004, CCRIF was formed in 2007 with the support of the World Bank to mitigate the short-term cash flow problems that smaller developing nations face after a natural disaster. CCRIF’s participants include the island nations that comprise the Caribbean Community (CARICOM) as well as non-CARICOM Central American nations. CCRIF operates as a mutual insurance company and was initially capitalized by member governments, the World Bank, and non-member nations providing grants. Premiums paid by member nations are proportional to the amount of risk that each nation transfers. This risk is then either retained or transferred to reinsurance markets. In the event of a natural disaster affecting one or more of CCRIF’s members, payouts are determined by parametric triggers. Should a disaster meet the predefined criteria, the payout is transferred to the treasuries of the recipient nations. The underlying logic behind CCRIF is that by spreading risk across multiple member nations, capital needs for paying claims are kept affordable for smaller economies that would otherwise struggle to insure themselves alone. In this way CCRIF’s framework provides an example of regional resiliency. Payouts occur quickly after an event takes place, thereby allowing its member states to take an accelerated path to recovery.

Pre-event risk reduction

The impact of insurance on resilience can be measured not only through post-event financial relief, but also pre-event risk reduction. The insurance industry should be seeking opportunities to partner with government risk managers and development entities to increase general risk awareness and influence smart regulation. The Insurance Institute for Business & Home Safety (IBHS) is an insurance industry-funded organization that is dedicated to reducing potential losses by strengthening homes and businesses. IBHS’s Fortified Homes program provides tangible steps for homeowners and contractors to build homes that can stand strong in a natural disaster. This program has helped create a more resilient building stock in hurricane-prone areas in the United States.

Another example is Build Change, a nonprofit organization that works directly with local communities to retrofit and rebuild homes and schools to withstand the stresses from hurricanes and earthquakes. Build Change has been working in Haiti since the 2010 earthquake, training homeowners, contractors, and public officials to not only rebuild a more resilient environment, but to increase local awareness and support for continuing efforts.

There are numerous examples where insurance can more directly impact risk mitigation efforts through partnerships with organizations like IBHS and Build Change, as well as direct outreach to government risk managers.

Case study: risk mitigation in Los Angeles

The protection gap looms especially large in the Golden State. The state as a whole remains severely uninsured as only 10.8 percent of the residential property insurance policies in 2015 had earthquake coverage (the figure drops to 5.2 percent for renters). By comparison, 33 percent of Californians had coverage at the time of the 1994 Northridge earthquake. Here, the industry has an important role to play in supporting risk-mitigation initiatives designed to reduce the impact earthquakes have on geographically vulnerable regions. An example of such initiatives is on display in the City of Los Angeles, which swept earthquake retrofit laws into effect in 2015. Under the current mayor, Eric Garcetti, additional measures have also been taken to protect Los Angeles’ water supply (88 percent crosses the San Andreas Fault line) as well as protect the region’s electric power grid. As part of the Garcetti admin-istration’s Resilience by Design program, the mayor’s office went as far as to call for the introduction of a seismic resilience bond to strengthen the city’s aqueducts, water storage, pipe network, and other critical water infrastructure. While earthquake coverage is slightly higher in the Los Angeles area than in the rest of California, the current administration has identified the expansion of earthquake insurance in neighborhoods where coverage rates are less than the California average as a necessary goal. Such measures are in progress to combat the impact of an event that the mayor describes as a question of “when,” not “if”.

Closing the gap

Closing the protection gap should be an immediate priority for any insurer wishing to stay relevant in a global economy that is becoming riskier. The impact of climate change on the frequency and severity of catastrophic events, coupled with the increasing concentration of people in the world’s most hazard-prone areas, means that the stakes are high. Without innovative leadership from the industry, communities will struggle to build resilience, and the costs will fall entirely on governments (i.e. taxpayers) and aid organizations. Opportunities already exist for insurance to be more engaged in directly solving the problem. Nonprofit organizations like Build Change and IBHS will have an increasingly important role to play in promoting risk mitigation strategies.

Closing the protection gap should be an immediate priority for any insurer wishing to stay relevant in a global economy that is becoming riskier. The impact of climate change on the frequency and severity of catastrophic events, coupled with the increasing concentration of people in the world’s most hazard-prone areas, means that the stakes are high. Without innovative leadership from the industry, communities will struggle to build resilience, and the costs will fall entirely on governments (i.e. taxpayers) and aid organizations. Opportunities already exist for insurance to be more engaged in directly solving the problem. Nonprofit organizations like Build Change and IBHS will have an increasingly important role to play in promoting risk mitigation strategies.

De-risking governments by providing post-event financial support, such as the NFIP reinsurance program, or creating new products like a seismic resilience bond, creates private market opportunities by expanding the risk/capital marketplace. Closing the protection gap helps build resilience, promotes sustainable, less risky behaviors, and ultimately helps save lives.

About the Author:

Liz Henderson leads the Catastrophe Risk Analytics group in Chicago for Aon's Reinsurance Solutions Analytics business. The group provides catastrophe modeling analysis and reinsurance placement support for our U.S. property casualty clients. Her specializations include providing risk management, consulting, and catastrophe modeling services to clients particularly in personal lines property, small commercial property and workers' compensation. Liz has recently been leading development on modernizing Catastrophe Risk Analytics client portal through Analytics Dashboards. Liz is a proud member of Aon's Diversity & Inclusion Council and she's committed to supporting inclusion at Aon every day.