How can banks get faster returns on investment in digital transformation?

Building a resilient workforce, People & Organisations, Financial Services

As Asia moves up the charts of the wealthiest regions in the world, the Asian ambition of banks now centres on a burgeoning segment of wealthy individuals and families. This ambition is further fuelled by the opportunity that changing demographics and increasing client sophistication provide to banks to differentiate themselves from competitors.

In the last few years, massive wealth transfers from baby boomers and digital savvy millennials drove wealth managers to ramp up digital platforms. The Covid-19 pandemic accelerated these changes as clients spent more time on devices than on interacting with Relationship Managers (RMs) in person.

Even while millions of dollars were being invested in digital transformation of private banks, compensation and benefits expenses kept rising as firms continued to hire client service teams led by Relationship Managers.

Between 2015 to 2020, the number of private banking RMs catering to the HNWI/UHNWI segments increased by 54%. There was also a 37% increase for the priority or mass affluent segment. This, when put in the context of the supply-side issues, wherein the lure of tech firms is pulling fresh hires away from financial services, has put immense additional cost pressures on banks, in addition to the cost of digital technology. Right now, it takes a three to five-year period for each dollar invested in digital to return to a bank’s bottom-line.

How can banks ensure that their investment in digital transformation has a faster run rate on savings?

The answer lies in reimagining the entire asset gathering and client servicing piece. This can be achieved by mapping the key moments in the client journey that can be positively impacted by digital or the human touch of a RM.

The challenge is that both digital and RMs are being made available for clients. However, an evolving client demographic means that most clients prefer digital self-service. Despite the preference, client satisfaction with digital channels in 2019 fell by 50% when compared to 2017. This led to banks quickly tapping into the bandwidth of RMs to cover any gaps in service to clients in addition to ramping up their digital portals.

If banks want to drive revenue and keep client team/RM-related costs in check, a data and analytics-based approach that provides a deep understanding of client personas will be essential. Aon’s client insight research suggests that about 75% of clients in Asia are “collaborators”— self-sufficient but need an RM to partner with them on their wealth management journey.

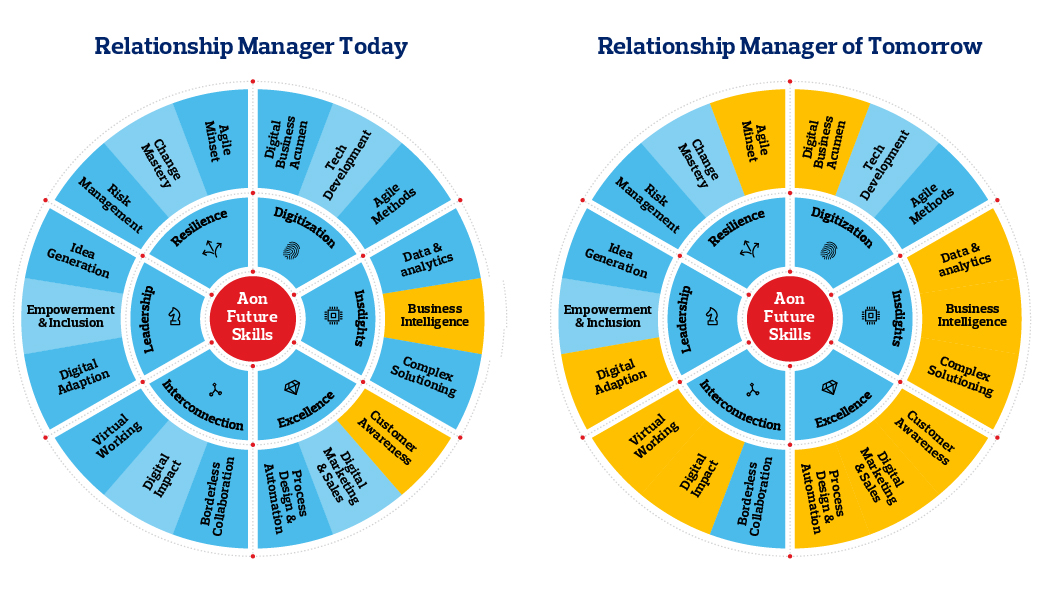

Three key things can ensure that banks hire the RM of the future.

- Hire agile RMs to ensure that they step in at key moments of the customer’s journey through digital platforms. An RM’s in-depth understanding of banking products and digital capabilities, along with their knowledge of customer sophistication levels can drive the right outcome for customers and banks.

- Newly hired RMs must display certain required behaviours for asset/revenue growth. This risk can be mitigated by creating success profiles for RMs based on mapping productivity data with the required RM behaviours and then using the right talent and rewards levers to build these skills in the existing talent pool.

- Cast the recruiting net beyond the traditional RM talent pool and onto areas such as other lines of business or middle offices. Assessing this talent pool for future skills and then putting them through a structured development journey can help to solve the supply-side problem with which banks are now grappling.

-