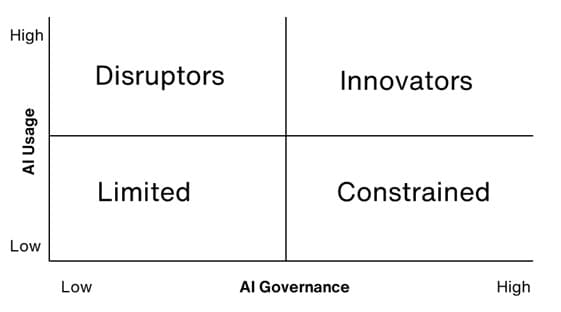

While it is too soon to say that there are any best AI governance practices, nine out of ten managers surveyed agree

that, at least for now, accountability is best supported by a strict human‑in‑the‑loop policy: AI‑generated

recommendations should always be reviewed before decisions are made. Many stipulate in their AI policy that they

don’t allow unmonitored decision-making or actions via AI within any business unit.

What are the next AI-related action steps for investors?

For investors, ensuring AI use is well-governed is not merely a technological or operational imperative; it is an

important step in enhancing resilience and positioning for success.

It’s important to note that AI uses and governance differ across the investment chain. For example, while investment

managers tend to be direct users of AI in multiple areas of their workflow, their clients—asset owners, such as

retirement funds, endowments and foundations are trying to figure out what their oversight responsibilities might

look like as indirect users. There may also be some direct use of AI by asset owners in areas such as pension

administration and member communication.

To oversee how AI is used, asset owners, supported by their investment advisors, may take the following 3 key steps:

1. Conduct due diligence regarding manager use and governance of AI.

2. Ask managers AI-related operational questions, for example:

- Do you use AI in your investment process and for which asset classes?

- What areas do you seek to improve with AI use?

- How significant do you view the risks and opportunities of AI to your firm?

- How do you verify / address potential bias in AI outputs and when and how does human oversight occur?

- Does your firm have governance practices such as an AI policy (either standalone or as part of cybersecurity),

protocols for handling data privacy in AI applications, guidelines for the responsible sourcing of data used in

AI models or formal training for staff on how to explain and interpret the use of AI?

3. Standardize AI-related factors as part of the manager selection and monitoring process.

Conclusion

AI use is fast becoming mainstream for asset managers. As adoption accelerates, strong governance must keep pace. The

firms that win will be those that embrace AI’s efficiencies while setting clear guardrails around its use, ensuring

transparency and accountability at every step. For asset owners, now is the time to formalize expectations, ask the

right questions, and strengthen oversight. Good AI governance is pivotal both for risk management and as a strategic

advantage in an increasingly crowded digital investment landscape.