May 21, 2024 7 mins

How to Navigate the EMEA Cyber Risk Insurance Market

As the cyber insurance landscape continues to evolve in EMEA, companies need actionable insights and solutions to strengthen their cyber risk strategies.

Key Takeaways

-

Despite heightened cyber security regulations and a notable surge in cyber and privacy incidents, cyber insurance pricing is expected to remain stable through 2024.

-

Proactively engaging with knowledgeable insurers will help companies protect against emerging cyber threats.

-

Risk managers can adopt four ways to make better cyber security policy decisions.

The dynamic cyber landscape is shaped by several factors — from heightened privacy and cyber security regulations and evolving privacy litigation culture to increasing ransomware events, the emergence of artificial intelligence (AI) and machine learning-driven cyberattacks. This reflects the growing complexity and severity of cyber risks.

Key trends shaping the EMEA cyber insurance market include:

-

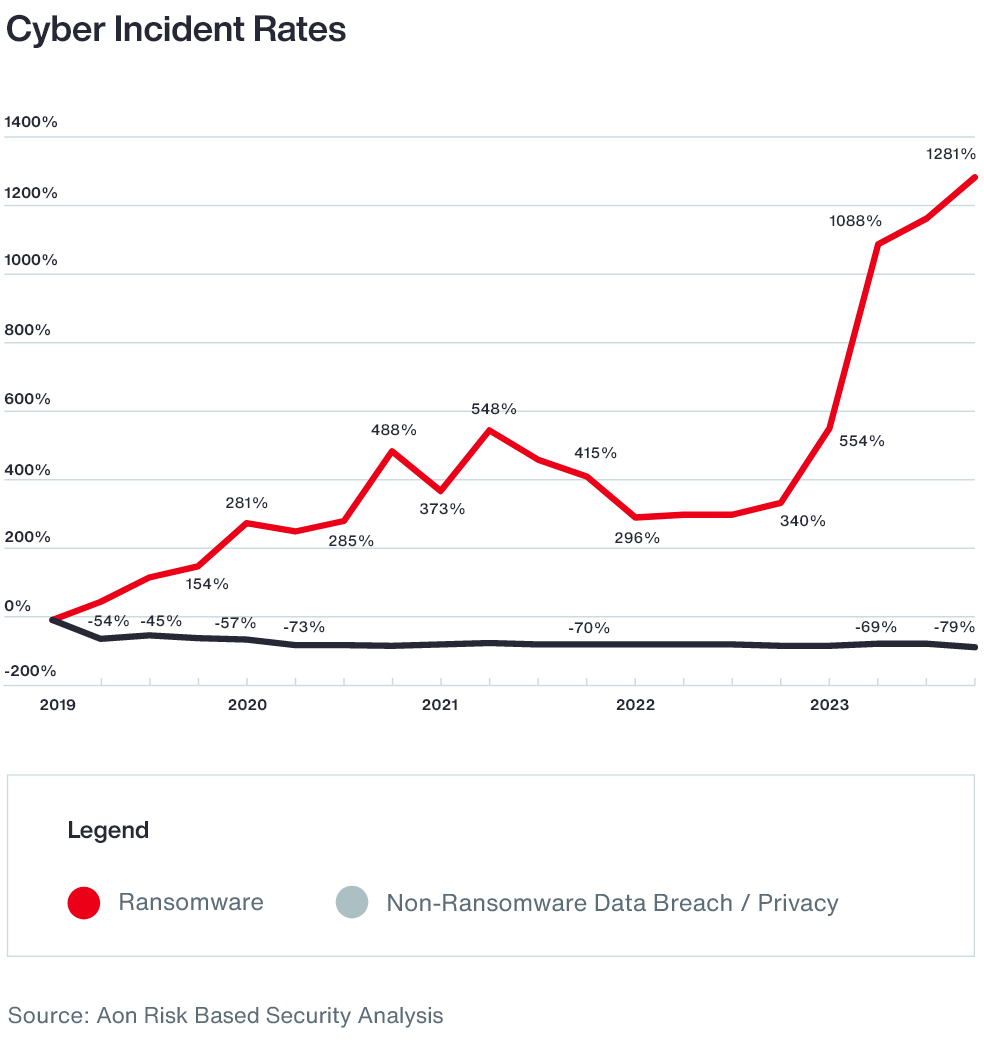

1. Surging ransomware attacks

- Ransomware attacks spiked drastically in the first half of 2023 and continued to escalate into Q4 2023. This not only disrupted businesses across business professional services, real estate/construction, and manufacturing, but also increased insurer losses.

- Ransomware activities will maintain their upward trajectory, posing persistent threats to organizations worldwide. The intersection of these cyber threats with new regulations makes way for agile responses from insurers and brokers alike.

-

2. Increasing Adoption of Artificial Intelligence

- The adoption of AI and machine learning also introduces novel risks and challenges, underscoring innovation and adaptation within the cyber insurance ecosystem.

- Several insureds view AI as not only a potential cyber security threat to be leveraged by bad actors, but also a tool to improve their own cyber security posture.

Against this backdrop, the regulatory landscape is faced with further evolution. Data privacy regulations are expected to come into effect globally, with the U.S. leading the charge. Additionally, with the European Union’s (EU) landmark AI Act1 and the EU NIS2 Directive on the horizon, cyber security in 2024 promises to be both exhilarating and demanding as it navigates uncharted terrain.

To adequately handle future uncertainty, you need to partner with a long-term insurer who knows your risk, pays claims reliably, and can tailor policy wording to suit your exposures and incident response plans.

Systemic Risk is a Top Concern for Insurers

Systemic risk continues to play an important role in the evaluation, scrutiny and, in some instances, restricted coverage offered for critical infrastructure, correlated events and war. Certain insurers restrict coverage on either a generalized or event-specific basis.

Since passing the first anniversary of Lloyd’s cyber war exclusion market bulletin,2 domestic insurers are starting to implement similar wording concepts (e.g., a compliant war and cyber operations exclusion must now be included in policies purchased through Lloyd’s). This has led to some confusion and market income loss.

“After years of discussion and negotiation, it seems the market has finally come to a landing with respect to the scope and wording of war and cyber operations exclusions, which is evident in the January 1st renewals,” says Pablo Constenla, Aon’s Head of Cyber Coverage and Claims for EMEA. “This highlights the importance of organizations partnering with insurers to review and secure the right limit and coverage.”

214%

Increase in ransomware activity in Q4 2023

YOY

Source: Aon Cyber Solutions

Buyer-Friendly Cyber Market Conditions Prevail

Despite a growing number of cyber incidents, heighted privacy regulation, as well as the increase in class actions (and the implementation of the European Representative Actions Directive), the EMEA’s buyer-friendly cyber market expanded due to new and returning insurers bringing in fresh capital and intensifying competition and businesses— ultimately strengthening cyber security.

7.3%

Decline in cyber premium rates in Q1 2024

YOY

Source: Aon Cyber Solutions internal benchmarking data

In 2023 and early 2024, organizations might have had more options for coverage if they could demonstrate a high-quality risk such as one that is:

- well-articulated around their cyber security resilience journey

- well-prepared with good risk information, no claims history, etc...

- well-protected around key security controls

This appears to have led to better business interruption coverage, more precise language based on claims experience and readiness from insurers to cooperate with organizations and more closely customize insurance programs according to specific needs.

Economic fluctuations, coupled with a shift in the geopolitical environment and widespread systemic cyber events, further shape the buyer-friendly cyber market.

“Organizations should make the most of the current favorable market conditions by carefully considering their cyber insurance buying strategy,” says Søren Stryger, Chief Broking Officer, Cyber Solutions, EMEA . “Doing so will not only optimize terms and conditions, but also build resilience for future market movements.”

Areas to watch carefully include supply chain attacks, silent attacks, more sophisticated regulatory fines, and penalties and changes in data protection litigation culture.

Even though cyber incidents are increasing, most cyber claims are resolved based on experience. “Insurers understand the complexity and uniqueness of each cyber claim,” Constenla explains. “Having an open mindset is crucial for the successful outcome.”

To avoid financial and reputational damage from cyber and privacy incidents, companies must adopt proactive cyber risk management practices and customized cyber insurance aligned with their cyber security strategy.

Navigate the Future Cyber Space with Confidence

Here are four ways to make better cyber policy decisions:

-

1. Build stability and bespoke solutions.

Now is the right time to review your policy, including new risks such as increased legalization. Understand changes and how different insurance policies work together to create stabilization and ensure coverage remains relevant.

-

2. Quantify your cyber risk.

With the evolution of AI technologies potentially being used for or against a business, it is important to understand existing risks and work toward insuring them appropriately. While the focus in previous years was on coverage, organizations can partner with insurers to drive conversations around:

- Wording

- Relevance

- 360 days consideration to salvage policy

-

3. Partner with the whole organization.

Cyber and privacy risk is a company risk. Work together with the entire business to effectively showcase controls — from the chief information security officer and privacy counsel to different teams across the organization.

-

4. Maintain the confidential nature of insurance policies.

Keep threat actors from knowing coverage information that can be used against the organization. Bad actors continue to threaten victims and demand ransom payments that are based on the client’s insurance coverage limits.

It is essential for risk managers to review the tools, technologies and procedures necessary to help combat cyber threats.

“Proactively engage with knowledgeable insurers and stay ahead of emerging threats,” advises Stryger. “This will allow risk managers to better protect their organization’s resilience against cyber risks.”

General Disclaimer

This material has been prepared for informational purposes only and should not be relied on for any other purpose. You should consult with your own professional advisors before implementing any recommendation or following the guidance provided herein. Further, the information provided, and the statements expressed are not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information and use sources that we consider reliable, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future.

All descriptions, summaries or highlights of coverage are for general informational purposes only and do not amend, alter or modify the actual terms or conditions of any insurance policy. Coverage is governed only by the terms and conditions of the relevant policy.

Terms of Use

The contents herein may not be reproduced, reused, reprinted or redistributed without the expressed written consent of Aon, unless otherwise authorized by Aon. To use information contained herein, please write to our team.

Aon's Better Being Podcast

Our Better Being podcast series, hosted by Aon Chief Wellbeing Officer Rachel Fellowes, explores wellbeing strategies and resilience. This season we cover human sustainability, kindness in the workplace, how to measure wellbeing, managing grief and more.

-

Podcast 23 mins

Better Being Series: Understanding Burnout in the Workplace -

Podcast 14 mins

Better Being Series: Why Nutrition Matters -

Podcast 10 mins

Better Being Series: Discover the ‘Blue Zones’ Where People Live Longer -

Podcast 20 mins

Better Being Series: Improving Your Financial Wellbeing -

Podcast 17 mins

Better Being Series: Are You Taking Care of Your Digital Wellbeing? -

Podcast 19 mins

On Aon Podcast: Better Being Series Dives into Women’s Health -

Podcast 25 mins

On Aon’s Better Being Series: Managing Loss and Grief

Aon Insights Series Asia

Expert Views on Today's Risk Capital and Human Capital Issues

-

Article 8 mins

Thriving in an Interconnected World: How the C-Suite Embraces Uncertainty -

Article 6 mins

Powering Progress: Collaborating to Build a Sustainable Future in Emerging Markets -

Article 5 mins

Building Business Resilience: Key Steps to Effectively Integrate Risk Management Across Your Organisation -

Article 7 mins

Why Humans Are the Essential Factor in the Success of Artificial Intelligence (AI) -

Article 5 mins

Leveraging Research and Expertise to Strengthen Your HR Strategy for 2025 and Beyond -

Article 5 mins

Managing Risk on the Energy Transition Journey -

Article 7 mins

The Role of Risk Management in the Age of Generative Artificial Intelligence -

Article 7 mins

Finding A Way In Asia Pacific's New Economic Reality -

Article 4 mins

Three Ways to Boost Value from Benefits: APAC Insights from LinkedIn

Aon Insights Series Pacific

Expert Views on Today's Risk Capital and Human Capital Issues

-

Article 3 mins

Article Template to Duplicate

Aon Insights Series UK

Expert Views on Today's Risk Capital and Human Capital Issues

-

Article 2 mins

Introduction: Clarity and Confidence to Act Now -

Article 11 mins

Navigating a New Age of Macroeconomic Uncertainty -

Article 3 mins

Making Better Decisions — A C-Suite Perspective -

Article 3 mins

Understanding the Dynamics of Today’s Workforce — Reward, Retain, Evolve -

Article 3 mins

Artificial Intelligence — Managing the Risk and Potential -

Article 10 mins

Unlocking Balance Sheet Value to Empower Your Business Strategy -

Article 3 mins

Navigating the Unpredictable: Aon’s Suite of Actionable Analytics -

Article 4 mins

Redefining Risk Capital as a Business Enabler: Veolia's Innovative Approach -

Article 9 mins

A Data-Driven Approach to Better Workforce Decisions -

Article 5 mins

The Importance of Pay Transparency -

Article 6 mins

How Human Capital Data Enhances Risk Management for Financial Institutions -

Article 4 mins

The Battle for Top Talent in the Professional Services Sector -

Article 5 mins

Insights on a Volatile World — Risk Factors That Businesses Need to be Monitoring

Client Trends 2025

Better Decisions Across Interconnected Risk and People Issues.

-

Article 3 mins

Acknowledging Our Complex Reality -

Article 10 mins

Trade in a Technology-Driven Future -

Article 9 mins

How AI and Workforce will Intersect: Navigating Risks and Opportunities -

Article 8 mins

Weather and Workforce: Employers Must Quantify the Risk -

Article 9 mins

Steering Trade and Supply Chains Amid Weather Challenges -

Report 13 mins

Trade Issues Confront Global Businesses on Multiple Fronts -

Report 19 mins

Technology is Driving Firms to Harness Opportunities and Defend Against Threats -

Report 19 mins

Climate Analytics Unlock Capital to Protect People and Property -

Report 14 mins

A Workforce in Transition Prepares to Meet a Host of Challenges

Construction and Infrastructure

The construction industry is under pressure from interconnected risks and notable macroeconomic developments. Learn how your organization can benefit from construction insurance and risk management.

-

Article 8 mins

How North American Construction Contractors Can Mitigate Emerging Risks -

Article 7 mins

Managing Construction Risks: 7 Risk Advisory Steps -

Article 7 mins

Unlocking Capacity and Capital in a Challenging Construction Risk Market -

Article 7 mins

Protecting North American Contractors from Extreme Heat Risks with Parametric -

Article 5 mins

How Climate Modeling Can Mitigate Risks and Improve Resilience in the Construction Industry -

Report 1 mins

Construction Risk Management Europe Report 2023 -

Article 8 mins

Parametric Can Help Mitigate Extreme Heat Risks for Contractors in EMEA

Cyber Resilience

Our Cyber Resilience collection gives you access to Aon’s latest insights on the evolving landscape of cyber threats and risk mitigation measures. Reach out to our experts to discuss how to make the right decisions to strengthen your organization’s cyber resilience.

-

Article 8 mins

Cyber and E&O Market Conditions Remain Favorable Amid Emerging Global Risks -

Article 7 mins

How to Navigate AI-Driven Cyber Risks -

Article 9 mins

Building Resilience in a Buyer-Friendly Cyber and E&O Market -

Article 11 mins

A Middle Market Roadmap for Cyber Resilience -

Article 7 mins

Lessons Learned from the CrowdStrike Outage: 5 Strategies to Build Cyber Resilience -

Article 8 mins

Responding to Cyber Attacks: How Directors and Officers and Cyber Policies Differ -

Article 6 mins

Why Now is the Right Time to Customize Cyber and E&O Contracts

Employee Wellbeing

Our Employee Wellbeing collection gives you access to the latest insights from Aon's human capital team. You can also reach out to the team at any time for assistance with your employee wellbeing needs.

-

Article 8 mins

Employer Strategies for Cancer Prevention and Treatment -

Article 6 mins

The Long-Term Care Conundrum in the United States -

Article 9 mins

Developing a Paid Leave Strategy That Supports Workers and Their Families -

Article 9 mins

4 Ways to Foster a Thriving Workforce Amid Rising Health Costs -

Article 9 mins

The Next Evolution of Wellbeing is About Performance -

Article 6 mins

Three Ways Collective Retirement Plans Support HR Priorities -

Article 9 mins

How the Right Employee Wellbeing Strategy Impacts Microstress and Burnout at Work -

Podcast 13 mins

On Aon Podcast: The Future of Healthcare: Key Factors Impacting Medical Trend Rates -

Article 7 mins

Making Wellbeing Part of a Company’s DNA -

Article 7 mins

A Comprehensive Approach to Financial Wellbeing

Environmental, Social and Governance Insights

Explore Aon's latest environmental social and governance (ESG) insights.

Q4 2023 Global Insurance Market Insights

Our Global Insurance Market Insights highlight insurance market trends across pricing, capacity, underwriting, limits, deductibles and coverages.

-

Article 12 mins

Q4 2023: Global Insurance Market Overview -

Article 13 mins

Top Risk Trends to Watch in 2024

Global Risk Management Survey

Better Decisions Across Interconnected Risk and People Issues.

-

Report 28 mins

A New Era of Converging Risks and Accelerating Disruption -

Article 1 mins

Top 10 Global Risks -

Article 1 mins

Industry Insights: Findings from Aon's Global Risk Management Survey -

Article 1 mins

Regional Results -

Article 41 mins

Country-Level Findings -

Report 5 mins

Methodology and Respondent Demographics

Regional Results

How do the top risks on business leaders’ minds differ by region and how can these risks be mitigated? Explore the regional results to learn more.

-

Article 12 mins

Rethinking Resilience: Addressing Asia Pacific’s Top Risks -

Article 10 mins

Turning Uncertainty into Opportunity: Managing Risk in the EMEA Region -

Article 10 mins

Latin America’s Risk Landscape: Turning Complexity into Competitive Advantage -

Article 10 mins

Rethinking Resilience: Navigating North America’s Evolving Risk Landscape

Impact Report 2025

Explore Aon's corporate sustainability impact and strategy.

-

Article 7 mins

Executive Summary -

Article 13 mins

Aon’s Environmental Sustainability -

Article 15 mins

Supporting Energy Resilience and a Transition to a Low-Carbon Economy -

Article 20 mins

Our Commitment to Our Colleagues -

Article 8 mins

Our Community Impact -

Article 10 mins

Governance -

Article 8 mins

Cyber and Data Security -

Article 11 mins

Redefining Resilience

Top 10 Global Risks

Trade, technology, weather and workforce stability are the central forces in today’s risk landscape.

-

Article 6 mins

Cyber Risk: Turning Uncertainty into Opportunity -

Article 7 mins

Business Interruption: Managing Risk in an Interconnected World -

Article 6 mins

Why Economic Slowdown is an Ongoing Risk for Organizations -

Article 8 mins

Navigating Regulatory and Legislative Change -

Article 5 mins

Increasing Competition Is Intensifying Risk for Organizations -

Article 7 mins

Commodity Price Risk and Material Scarcity: An Escalating and Complex Risk -

Article 9 mins

Supply Chain or Distribution Failure: Navigating the New Normal -

Article 5 mins

Damage to Reputation or Brand: A Critical Risk -

Article 6 mins

Geopolitical Volatility: Preparing for the Unpredictable -

Article 6 mins

Cash Flow and Liquidity Risk: A Rising Challenge

Industry Insights

These industry-specific articles explore the top risks, their underlying drivers and the actions leaders are taking to build resilience.

-

Article 9 mins

Building Resilience to Support Growth in Construction and Real Estate -

Article 10 mins

Managing Risk and Unlocking Opportunity in the Food, Agribusiness and Beverage Industry -

Article 8 mins

Adapting to Disruption: How Financial Institutions are Reframing Risk -

Article 10 mins

Turning Risk into Resilience in the Industrials and Manufacturing Industry -

Article 11 mins

Navigating Risk in Insurance: Turning Complexity into Competitive Advantage -

Article 10 mins

Navigating Risk in Life Sciences: Building Resilience to Support Growth -

Article 11 mins

Navigating Volatility in Natural Resources: Risk Management as a Value Driver -

Article 10 mins

Navigating Risk in Transportation and Logistics: Gearing Up for Big Transitions -

Article 9 mins

Technology, Media and Communications: Rethinking Risk in a Shifting Landscape

Human Capital Analytics

Our Human Capital Analytics collection gives you access to the latest insights from Aon's human capital team. Contact us to learn how Aon’s analytics capabilities helps organizations make better workforce decisions.

-

Article 35 mins

5 Human Resources Trends to Watch in 2025 -

Article 13 mins

Medical Rate Trends and Mitigation Strategies Across the Globe -

Article 9 mins

3 Strategies to Help Avoid Workers Compensation Claims Litigation -

Podcast 15 mins

On Aon Podcast: Using Data and Analytics to Improve Health Outcomes -

Article 14 mins

How Technology Will Transform Employee Benefits in the Next Five Years -

Podcast 18 mins

On Aon Podcast: Technology Impacting the Future of Health and Benefits -

Article 10 mins

Designing Tomorrow: Personalizing EVP, Benefits and Total Rewards

Human Capital Quarterly Insights Briefs

Read our collection of human capital articles that explore in depth hot topics for HR and risk professionals, including using data and analytics to measure total rewards programs, how HR and finance can better partner and the impact AI will have on the workforce.

-

Article 12 mins

Total Rewards Strategies That Drive Business Outcomes -

Article 35 mins

5 Human Resources Trends to Watch in 2025 -

Article 20 mins

5 Ways HR Can Partner with Finance to Drive Growth -

Article 15 mins

How Artificial Intelligence is Transforming Human Resources and the Workforce -

Article 15 mins

Five Big Human Resources Trends to Watch in 2024 -

Article 10 mins

Designing Tomorrow: Personalizing EVP, Benefits and Total Rewards -

Article 10 mins

How Data and Analytics Can Optimize HR Programs -

Article 15 mins

Get Ready for the Top 5 HR Trends in 2023

Insights for HR

Explore our hand-picked insights for human resources professionals.

-

Article 7 mins

COVID-19 has Permanently Changed the Way We Think About Wellbeing -

Article 10 mins

How Data and Analytics Can Optimize HR Programs -

Article 7 mins

Case Study: The LPGA Unlocks Talent Potential with Data -

Article 10 mins

Navigating the New EU Directive on Pay Transparency -

Article 6 mins

Rethinking Your Total Rewards Programs During Mergers and Acquisitions

Workforce

Our Workforce Collection provides access to the latest insights from Aon’s Human Capital team on topics ranging from health and benefits, retirement and talent practices. You can reach out to our team at any time to learn how we can help address emerging workforce challenges.

-

Article 8 mins

Weather and Workforce: Employers Must Quantify the Risk -

Article 12 mins

Total Rewards Strategies That Drive Business Outcomes -

Article 8 mins

AI and Workforce Skills: Who Should Act and Why Now? -

Article 19 mins

3 Strategies to Promote an Inclusive Environment and Bridge the Gender Gap -

Article 8 mins

2025 Salary Increase Planning Tips -

Article 12 mins

People Risks Are Rising: Here’s How U.S. Benefits Are Stepping Up -

Article 8 mins

Employer Strategies for Cancer Prevention and Treatment -

Article 6 mins

Taking a Data-Led Approach to Job Architecture to Accelerate Pay Transparency -

Podcast 12 mins

Better Being Series: Building Sustainable Performance in a Multi-Generational Workforce -

Article 7 mins

Key Trends in U.S. Benefits for 2025 and Beyond -

Article 7 mins

Why Pay Transparency Demands a Total Rewards Lens -

Article 9 mins

4 Ways to Foster a Thriving Workforce Amid Rising Health Costs

Mergers and Acquisitions

Our Mergers and Acquisitions (M&A) collection gives you access to the latest insights from Aon's thought leaders to help dealmakers make better decisions. Explore our latest insights and reach out to the team at any time for assistance with transaction challenges and opportunities.

-

Article 6 mins

Rethinking Your Total Rewards Programs During Mergers and Acquisitions -

Article 9 mins

Organizational Design and Talent Planning are Key to M&A Success -

Article 5 mins

Project Management for HR: The Secret Behind a Successful M&A Deal -

Article 8 mins

Cultural Alignment Planning Drives M&A Success -

Report 1 mins

A Guide to Maximizing Value in Post-Merger Integrations -

Report 2 mins

The ABC's of Private Equity M&A: Deal Flow Impacts of Al, Big Tech and Climate Change -

Article 11 mins

The Silver Lining on M&A Deal Clouds: M&A Insurance Insights from 2023

Natural Resources and Energy Transition

The challenges in adopting renewable energy are changing with technological advancements, increasing market competition and numerous financial support mechanisms. Learn how your organization can benefit from our renewables solutions.

-

Article 4 mins

5 Steps for Successful Carbon Accounting Verification -

Article 6 mins

AI Innovations in Renewable Energy: Transforming the Sector -

Article 11 mins

Securing Human Capital in Natural Resources -

Article 6 mins

Decarbonizing Construction for a Low-Emission Future

Navigating Volatility

How do businesses navigate their way through new forms of volatility and make decisions that protect and grow their organizations?

Parametric Insurance

Our Parametric Insurance Collection provides ways your organization can benefit from this simple, straightforward and fast-paying risk transfer solution. Reach out to learn how we can help you make better decisions to manage your catastrophe exposures and near-term volatility.

-

Article 10 mins

How Public Entities and Businesses Can Use Parametric for Emergency Funding -

Article 6 mins

Parametric Insurance: A Complement to Traditional Property Coverage -

Article 8 mins

Using Parametric Insurance to Match Capital to Climate Risk -

Article 6 mins

Using Parametric Insurance to Close the Earthquake Protection Gap -

Article 5 mins

How Technology Enhancements are Boosting Parametric

Pay Transparency and Equity

Our Pay Transparency and Equity collection gives you access to the latest insights from Aon's human capital team on topics ranging from pay equity to diversity, equity and inclusion. Contact us to learn how we can help your organization address these issues.

-

Article 6 mins

Taking a Data-Led Approach to Job Architecture to Accelerate Pay Transparency -

Article 19 mins

3 Strategies to Promote an Inclusive Environment and Bridge the Gender Gap -

Report 1 mins

The 2024 North America Pay Transparency Readiness Study -

Article 10 mins

How Financial Institutions can Prepare for Pay Transparency Legislation -

Article 8 mins

Pay Transparency Can Lead to Better Equity Across Benefits -

Article 12 mins

Understanding and Preparing for the Rise in Pay Transparency -

Podcast 14 mins

On Aon Podcast: Understanding Pay Transparency Regulations -

Article 10 mins

Navigating the New EU Directive on Pay Transparency -

Article 6 mins

To Disclose Pay or Not? How Companies are Approaching the Pay Transparency Movement -

Podcast 19 mins

On Aon Podcast: Better Being Series Dives into Women’s Health -

Article 11 mins

Advancing Women’s Health and Equity Through Benefits and Support

Property Risk Management

Forecasters are predicting an extremely active 2024 Atlantic hurricane season. Take measures to build resilience to mitigate risk for hurricane-prone properties.

-

Article 8 mins

Florida Hurricanes Not Expected to Adversely Affect Property Market -

Article 10 mins

Build Resilience for an Extremely Active Atlantic Hurricane Season -

Article 4 mins

Four Steps to Develop Strong Property Risk Coverage in a Hardening Market -

Podcast 16 mins

On Aon Podcast: Navigating and Preparing for Catastrophes -

Article 6 mins

Parametric Insurance: A Complement to Traditional Property Coverage -

Article 4 mins

Navigating Climate Risk Using Multiple Models and Data Sets -

Article 5 mins

Rising Losses From Severe Convection Storms Mostly Explained by Exposure Growth -

Article 6 mins

Using Parametric Insurance to Close the Earthquake Protection Gap

Technology

Our Technology Collection provides access to the latest insights from Aon's thought leaders on navigating the evolving risks and opportunities of technology. Reach out to the team to learn how we can help you use technology to make better decisions for the future.

-

Article 9 mins

How AI and Workforce will Intersect: Navigating Risks and Opportunities -

Article 23 mins

The AI Data Center Boom: Strategies for Sustainable Growth and Risk Management -

Article 8 mins

AI and Workforce Skills: Who Should Act and Why Now? -

Article 7 mins

How Technology is Transforming Open Enrollment in the U.S. -

Article 15 mins

Navigating Cyber Risks in EMEA: Key Insights for 2025 -

Article 7 mins

How to Navigate AI-Driven Cyber Risks -

Article 15 mins

How Artificial Intelligence is Transforming Human Resources and the Workforce -

Podcast 9 mins

On Aon Podcast: How has CrowdStrike Changed the Cyber Market? -

Article 18 mins

5 Ways Artificial Intelligence can Boost Claims Management -

Article 12 mins

Navigating AI-Related Risks: A Guide for Directors and Officers -

Article 5 mins

How Technology Enhancements are Boosting Parametric -

Article 7 mins

How to Futureproof Data and Analytics Capabilities for Reinsurers

Trade

Our Trade Collection gives you access to the latest insights from Aon's thought leaders on navigating the evolving risks and opportunities for international business. Reach out to our team to understand how to make better decisions around macro trends and why they matter to businesses.

-

Article 10 mins

Trade in a Technology-Driven Future -

Podcast 9 mins

Special Edition: Global Trade and its Impact on Supply Chain -

Article 8 mins

The Evolving Threat of Cargo Theft: 5 Key Mitigation Strategies -

Report 1 mins

Findings from Aon's Global Risk Management Survey | Tenth Edition -

Article 4 mins

Four Steps to Develop Strong Property Risk Coverage in a Hardening Market -

Article 14 mins

Cutting Supply Chains: How to Achieve More Reward with Less Risk -

Article 9 mins

Driving Private Equity Value Creation Through Credit Solutions -

Article 7 mins

4 Steps to Help Take Advantage of a Buyer-Friendly Directors' & Officers' Market -

Article 8 mins

Managing Reputational Risks in Global Supply Chains -

Article 8 mins

How an Outsourced Chief Investment Officer Can Help Improve Governance and Manage Complexity -

Article 8 mins

Decarbonizing Your Business: Finding the Right Insurance and Strategy -

Article 8 mins

Reputation Analytics as a Leading Indicator of ESG Risk

Transaction Solutions Global Claims Study

Better Decisions Across Interconnected Risk and People Issues.

-

Report 5 mins

Chapter 1: Author’s Note & Executive Summary -

Report 8 mins

Chapter 2: North America: Highlights, Claims Severity and Frequency -

Report 3 mins

Chapter 3: North America: Breach Type and Notification -

Report 24 mins

Chapter 4: North America: Industry Sectors and Trends -

Report 5 mins

Chapter 5: North America: Tax Insurance Claims -

Report 5 mins

Chapter 6: EMEA: Highlights and Introduction -

Report 9 mins

Chapter 7: EMEA: Claim Frequency and Metrics -

Report 7 mins

Chapter 8: EMEA: Notifications by Target Location and Claims Severity and Payment Trends -

Report 10 mins

Chapter 9: EMEA: Breach Types and Trends -

Report 7 mins

Chapter 10: EMEA: Case Law, Insurer Survey, Claims Handling and Tax -

Report 6 mins

Chapter 11: APAC: Asia -

Report 9 mins

Chapter 12: APAC: Pacific

Weather

With a changing climate, organizations in all sectors will need to protect their people and physical assets, reduce their carbon footprint, and invest in new solutions to thrive. Our Weather Collection provides you with critical insights to be prepared.

-

Article 9 mins

Steering Trade and Supply Chains Amid Weather Challenges -

Podcast 9 mins

On Aon Podcast: Climate Impact on the Property and Casualty Market -

Alert 14 mins

L.A. Wildfires Highlight Urgent Need for Employee Support and Business Resilience -

Report 3 mins

2026 Climate and Catastrophe Insight -

Article 10 mins

How Public Entities and Businesses Can Use Parametric for Emergency Funding -

Podcast 12 mins

On Aon Podcast: Tackling Climate Risk to Build Economic Resilience -

Article 5 mins

Understanding Freeze Risk in a Changing Climate -

Podcast 9 mins

On Aon Podcast: Climate Science Through Academic Collaboration -

Article 6 mins

How Companies Are Using Climate Modeling to Improve Risk Decisions -

Article 8 mins

Using Parametric Insurance to Match Capital to Climate Risk -

Article 9 mins

Record Heatwaves: Protecting Employee Health and Safety

Workforce Resilience

Our Workforce Resilience collection gives you access to the latest insights from Aon's Human Capital team. You can reach out to the team at any time for questions about how we can assess gaps and help build a more resilience workforce.

More Like This

-

Article 9 mins

Insurers’ Opportunities in M&A: The Rise of Hybrid Growth Pathways

As insurance consolidation becomes more selective, insurers are looking beyond full acquisition as the default route to growth. Hybrid pathways may provide capital-efficient access to capabilities and talent, while requiring careful management of governance, execution and alignment risks.

-

Article 17 mins

Insurers’ Opportunities in M&A: When Buying Fits, When Building Wins

Insurers’ growth decisions are entering a more complex phase. As markets soften, capital costs rise and structured volatility pressures balance sheets, insurers are reassessing when consolidation creates real value — and when organic or alternative strategies may deliver better outcomes.

-

Article 8 mins

People Mobility in a Complex Global Environment

International employee and expat assignments remain popular despite headwinds. Employers looking to develop their employees’ skills and distribute talent can take advantage of the opportunities revealed by these challenges.

-

Article 8 mins

Healthcare Cost Increases Show No Signs of Slowing: What Employers Can Do

While the current environment is challenging, there are new options and strategies to contain costs and support employees.

-

Article 8 mins

SPACs Return: Why D&O Risk Management Must Step Up

SPACs are staging a comeback, but the risks that surrounded them in prior cycles remain. The challenge is to lead with proactive, strategic risk transfer that keeps stakeholders and balance sheets protected in a fast-evolving landscape.

-

Article 4 mins

Responding to Retirement Plan Complexity: A Guide for Mid-Market Employers

Employee retirement plans are getting more complex. Mid-market employers with lean HR teams must maintain consistent compliance and governance processes before small issues turn into costly corrections, penalties or employee trust issues.

-

Article 8 mins

How AI and Data are Transforming Employee Benefits Platforms

Employee benefits and total rewards platforms are redefining the employee experience through the combination of connected data, intelligent delivery and new technology. This trend is fundamentally changing how employees understand, access and use their benefits.

-

Article 4 mins

Casualty Risk Is Rewriting Balance Sheet Exposure

Liability severity is rising, volatility is increasing and many companies are retaining more casualty risk than they were a decade ago – often without changing how that exposure is measured, financed or reflected in capital decisions.

-

Article 10 mins

Cyber Risk is Growing Faster Than Risk Transfer

Cyber investment has grown rapidly, but insurance remains a marginal share of total cyber spend. As cyber losses drive larger operational and financial outcomes, many organizations continue to retain significant volatility on their balance sheets.

-

Article 2 mins

Defined Contribution in 2026: Rethinking the DC Operating Model

People are living longer and defined contribution plans play a central role in retirement security. This report explores what's changing and how employers can adapt to deliver better outcomes for their workforces.

-

Article 10 mins

Navigating Risk Across the Clean Energy Lifecycle from Design to Decommissioning

Clean energy investment is rising, but so are delivery, performance and financial risks. Scaling wind, solar and storage depends on lifecycle resilience that integrates people, engineering standards and risk transfer from design through long-term operations.

-

Article 9 mins

Hull and Machinery Risk: How Technical Management and Execution Shape Outcomes

Global shipowners and operators face increasing complexity from geopolitical tensions, older fleets, volatile weather, crewing challenges and evolving regulations. Disciplined technical management is now more important to loss performance, resilience and long-term operating strength.

-

Article 11 mins

AI Isn’t the Differentiator. Workforce Readiness Is

AI is rapidly reshaping how work gets done and where value is created, yet many organizations are not translating their investment into business outcomes. Closing the gap between deployment and impact requires a focus on workforce readiness and aligning people strategy to performance.

-

Article 8 mins

Why Third-Party Cyber Risk is a Balance Sheet Issue

Many organizations assume contracts or insurance transfer third-party cyber risk until a disruption proves otherwise. Limiting financial fallout requires treating third-party exposure as a capital and resilience issue, with direct implications for earnings, cash flow and balance sheets.

-

Article 4 mins

Aon 2025/26 Global Pension Risk Survey

Explore how pension sponsors and leaders are responding to investment volatility, the latest regulations and operational pressures in Aon’s 2025–26 Global Pension Risk Survey.

-

Article 4 mins

New Strategies to Manage Rising Pharmacy Costs

Specialty drugs and GLP 1s are on the rise, changing the landscape of employee pharmacy benefits. Discover new strategies to better understand and manage pharmacy costs.

-

Article 5 mins

Four Considerations for Evolving Work with AI

Many companies face pressure to shrink workforces, but people‑first strategies can realize AI’s value while preserving strength and talent. Explore workforce design that empowers employees and unlocks the full value of AI.

-

Article 4 mins

Q&A: How Are Employers Supporting High-Cost Claimants While Managing Costs?

High-cost claimants continue to drive a disproportionate share of healthcare spend and volatility. Aon’s 2026 Health Survey shows how employers are responding, and where there are opportunities to manage costs without eroding support for employees in the future.

-

Article 13 mins

Tax Credit and Credit Insurance as Financing Enablers for U.S. Digital Infrastructure

Data centers, as part of U.S. digital infrastructure, face a tighter power market as clean energy tax credits become binary and time-bound.

-

Article 11 mins

Managing Renewable Construction Claims with Confidence

Construction-phase claims are rising as renewable projects grow larger, more complex and more exposed. Understanding where risk concentrates and how earlier, integrated decisions can reduce loss is central to delivery certainty, financing confidence and long-term insurability.

-

Article 5 mins

You Paid for AI Cyber Protection. Have You Priced What Happens When it is Wrong?

AI-driven cyber controls promise speed and precision, but when high-privilege automation is wrong or manipulated the real risk shows up on your P&L in your governance and at your next renewal.

-

Article 6 mins

Why 2026 Hurricane Preparedness Requires More Than a Forecast

A quieter 2026 hurricane season is possible, but risk remains. North American organizations, however, have a window to strengthen resilience. Combining exposure data with real-time analytics, claims readiness and resilience measures can help provide a strategic advantage for protecting assets.

-

Article 6 mins

Surplus Trust Assets: Trap or Opportunity?

As pension funding levels rise, surplus assets increasingly represent both opportunity and risk. A strategic framework for effective surplus decision making outlines how sponsors can evaluate durability, constraints and efficiency before pursuing any surplus strategy.

-

Article 6 mins

Preparing HR for the Next Phase of Pay Transparency

Momentum is building for pay transparency. As regulations emerge, employers are shifting their focus to communications and manager training, with a growing number viewing pay transparency as a strategic differentiator.

-

Article 8 mins

Demystifying Retirement Management for Multinational Employers

For multinational employers, global retirement management turns shared principles into consistent governance. This can result in improved retirement outcomes across countries.

-

Article 7 mins

How Can HR and the C‑Suite Align on Healthcare Costs?

Rising healthcare costs are an enterprise issue for employers. Organizations know they need to take urgent action but often lack alignment on how. Understanding C-Suite perspectives and learning how to collaborate is critical.

-

Article 15 mins

Evaluating Labor-Friendly Investment Strategies for Taft-Hartley Plans

Taft Hartley plans sit at the intersection of fiduciary duty and labor priorities. As interest in labor friendly investments grows, plan fiduciaries must only consider them while remaining firmly grounded in ERISA requirements.

-

Article 5 mins

The Risk You Already Own: Financing Digital Asset Exposure with a Captive

As digital asset exposure scales faster than most institutions’ risk frameworks, leading firms are using captives to turn unstructured retention into deliberate, capital-efficient strategy.

-

Article 8 mins

Why the Aging Workforce Demands a New Employer Strategy

As people work longer, employers that connect talent, health and retirement strategies will be best positioned to protect critical skills, manage health costs and avoid unplanned workforce exits.

-

Article 13 mins

AI Risk 2026: What Business Leaders Need to Know

The accelerating role of artificial intelligence in organizational decision making in 2026 is redefining exposure — from fraud to operational resilience. Leaders must strengthen controls, build clear accountability, and ensure their risk and insurance programs keep pace with AI‑driven threats.

-

Article 5 mins

Managing Global Benefits During Divestiture

As more organizations divest non-core operations, a critical challenge has emerged — establishing fit-for-purpose, cost-effective employee benefits for newly formed businesses in compressed timeframes. Effective solutions exist that simplify and accelerate implementation.

-

Article 5 mins

A New Pension Roadmap for Plan Sponsors

Defined benefit (DB) pension plan management has entered a new era. Learn more about the different tools and approaches plan sponsors need to meet their long-term goals.

-

Article 11 mins

Bridging the Gap: Solutions for Managing Construction-to-Operation Transition Risk

Construction-to-operation transitions are rarely seamless. Without clear responsibilities, precise handover definitions and aligned insurance structures, critical risks can fall through the cracks — but early coordination can help.

-

Article 9 mins

Exploring the DC OCIO Model

DC OCIO can save plan sponsors time, lessen fiduciary risk, and deliver potential fee savings all with the goal of enhancing participant outcomes

-

Article 28 mins

Q1 2026: Global Insurance Market Overview

Buyer friendly conditions continued into Q1 2026, underpinned by strong insurer performance and capacity availability, while rising geopolitical risks and other structural pressures introduced greater complexity beneath the surface.

-

Article 5 mins

Liquidity Under Pressure: Capital Allocation Decisions in the Middle Market

Rising costs, tighter insurance markets and more synchronized volatility are reshaping how North American middle market CFOs think about liquidity. The challenge is not just how much cash to hold but how to allocate it effectively under pressure.

-

Article 5 mins

4 Ways Analytics are Redefining North American Nat Cat Resilience

Natural catastrophe risk is now a persistent, financially material challenge for North American organizations. Advanced analytics help risk leaders quantify volatility, align decisions with risk appetite and strengthen resilience amid uncertainty.

-

Article 13 mins

Beyond Traditional Markets: Unlocking Alternative Risk Capital Solutions

Alternative risk capital solutions are increasingly important as organizations face complex, capital-intensive exposures and capacity constraints. Advances in modeling and diagnostics now help investors participate with confidence, supporting stronger resilience.

-

Article 9 mins

Pay Transparency Is Coming for Insurance. The Question Is: Are You Ready – or Just Hoping to Be?

Pay transparency is no longer a future consideration for insurers – it is a fast‑approaching test of governance, data discipline and leadership credibility. While the EU Pay Transparency Directive is the immediate trigger, its implications are global

-

Article 8 mins

Reputation as a Value Driver: Strengthening Resilience in Oil & Gas

Oil and gas companies face heightened scrutiny from governments, regulators, investors and consumers amid escalating geopolitical tensions. In this environment, reputational resilience is critical to protecting value, securing insurance and maintaining trust as energy security takes priority.

-

Article 11 mins

The AI Governance Frontier in Investment Management

Based on responses from 125+ investment managers, it’s clear that AI use in today’s market is now becoming mainstream and an AI governance maturity curve is emerging.

-

Article 9 mins

Building Tomorrow’s Grid: Managing Extreme Heat Risk in a Warming World

Extreme heat from climate change is increasingly threatening U.S. energy supply and reliability – forcing energy companies to take steps to safeguard operations and meet rising demand.

-

Article 11 mins

Natural Catastrophe Exposure: A Critical Inflection Point for Digital Infrastructure

Natural catastrophe risk is becoming a defining constraint of digital infrastructure development. Early planning decisions can make or break insurability — dictating how facilities withstand extreme weather and secure insurance capacity in a rapidly expanding market.

-

Article 5 mins

Converging Geopolitical and Enterprise Risks in Energy: What Leaders Need to Anticipate Now

Learn how energy leaders can map geopolitical shocks, align risk and compliance and use scenario modeling to build resilient, opportunity-ready portfolios.

-

Article 8 mins

When an Employee Benefits Captive is the Right Solution

Amid rising costs and a desire for more health data insights, companies are increasingly turning toward captive arrangements for their employee benefits. Here are the drivers of this movement, and how employers can decide if a captive is right for their employee benefits.

-

Article 5 mins

How AXA XL Transformed into a Skills-Based Organization

AXA XL, a subsidiary of the insurer and reinsurer AXA, wanted to capitalize on the talent they had in their organization in the face of a complex series of challenges. Working with Aon, AXA XL was able to future-proof its organization and ensure it can meet future workforce needs.

-

Article 7 mins

Global Growth for the Future: Metals and Mining

Mining is essential to global growth, yet rising demand, capital challenges, workforce shifts and geopolitical pressure are reshaping the sector. Leaders must strengthen capital, talent, technology and ESG resilience to meet future needs.

-

Article 11 mins

Clarity in the Era of Megaprojects: Rethinking Performance Security

As megaprojects scale and risk capital tightens, clarity has become central to effective performance security. Understanding how surety capacity, performance bonds, bank guarantees, instruments and regional requirements interact helps preserve liquidity, protect margins and deliver complex projects.

-

Article 6 mins

Measuring What Matters: Culture as the Foundation of AI Readiness

As AI transforms everyday work and skills, establishing a strong organizational culture helps build the employee trust needed to openly navigate new tools and embrace change as an opportunity for growth.

-

Article 10 mins

Reimagining Primary Care Through Collaboration

Aon Accelerate Lab insights on strengthening primary care as the coordinating hub of employer healthcare to improve access, outcomes and employee experience.

-

Article 13 mins

Three Roles to Build Insurance’s Next-Generation Workforce

As automation, climate risk, and shifting workforce expectations reshape insurance, building a future-fit talent strategy is now the industry’s defining challenge.

-

Article 5 mins

Property Risk in Natural Resources: The Shift from Severity to Duration

Climate volatility, asset concentration and extended rebuild timelines are reshaping property risk in natural resources. The defining exposure is no longer just how large a loss could be, but how long disruption could last and how that volatility flows through the balance sheet.

-

Article 14 mins

Building Bankable, Resilient Data Centers: From Site to Operation

Data center spending will reach $6.7 trillion by 2030, according to McKinsey.<sup>1</sup> With significant capital on the line, facilities demand a new lifecycle approach to risk that strengthens bankability, protects schedules and delivers operational resilience from day one.

-

Article 5 mins

What Multinational Employers Need to Know About GLP-1s

GLP-1 medicines for weight loss are increasingly popular in the U.S., prompting employers to consider coverage for employees. While not as common yet globally, GLP-1s spark a broader discussion around using data and analytics to identify health risks and address obesity as a disease.

-

Article 5 mins

Defensible Casualty Decisions in a Volatile, Data-Heavy World

As casualty volatility increases and financial scrutiny intensifies, risk leaders must do more than structure insurance programs. They must quantify and communicate how limits, retentions and program design align with enterprise risk tolerance and capital strategy.

-

Article 4 mins

Pooled Employer Plans as a Strategic Differentiator, with Saalex Corporation

Saalex, a U.S.-based government contractor, understands the value of employee benefits in attracting and retaining top talent. After a complete review of benefits, they were interested in the cost savings, administrative efficiencies and added benefits of a pooled employer program.

-

Article 4 mins

How to Uncover Hidden Costs in Employee Retirement Plans

Uncovering hidden costs is essential, not just for today’s balance sheet, but for securing the financial future of organizations and their retirees.

-

Article 8 mins

How AI, Cost Pressures and Reskilling are Transforming Talent Strategies

AI acceleration, rising healthcare costs and changes to workforce skills are transforming organizations. Our analysis of financial services, life sciences and technology companies provides insights on how to redesign roles, reskill at scale and reimagine talent strategies to stay competitive.

-

Article 6 mins

Strategies for Closing the Gender Retirement Pay Gap

Addressing the retirement pay gap issue between men and women starts with first acknowledging it exists. Then companies can conduct further analysis and adjust their benefit plans accordingly.

-

Article 10 mins

Unlock the Potential of Alternative Investments with an Outsourced Chief Investment Officer

Avoid limiting a portfolio’s capacity based on the capabilities or bandwidth of an existing process by working with the right partner.

-

Article 10 mins

Industrials and Manufacturing: A Risk Management Approach to Transform Workforce Risk into Workforce Resilience

Workforce-related risks — spanning health, benefits, safety systems, and data and analytics — are not just operational concerns but strategic drivers. When activated, they positively shape the total cost of risk and long-term resilience for industrials and manufacturing organizations.

-

Article 8 mins

Navigating the DB Pension Endgame: Lessons from Global Leaders

Rising longevity, shifting demographics and ongoing regulatory reform are reshaping defined benefit pension strategies. As legacy plans wind down, lessons from mature markets offer practical guidance for managing the final stage of a pension scheme’s journey: the endgame.

-

Article 7 mins

Managing Technological Risk in the Age of Advanced Gas Turbines

As the digital economy accelerates, driven by AI and cloud computing, the U.S. power sector faces a new era of demand. Advanced gas turbines are at the heart of this transformation, but their rapid evolution brings complex risks.

-

Article 24 mins

Q4 2025: Global Insurance Market Overview

Soft market conditions, ample capacity and heightened competition continued across most geographies and lines in Q4 — giving insurance buyers opportunities to secure better pricing, improve terms and expand coverage.

-

Article 17 mins

2026 P&C Outlook: Navigating Volatility, Unlocking Growth

A dynamic and interconnected property & casualty risk landscape persists in 2026. However, the insurance market presents ample capacity and opportunities for buyers. Yet, increasing volatility means the window to build long-term resilience is time sensitive in advance of the next market turn.

-

Article 9 mins

Policy Alert: New U.S. Executive Order on Artificial Intelligence – Aon Tips for Better Risk Capital Decisions

On December 11, 2025, U.S. President Donald J. Trump released a new Federal Executive Order — the latest effort towards the aggressive promotion of U.S. AI leadership and away from a fragmented, state-by-state regulatory model.

-

Article 10 mins

Retirement Resilience in FAB: Inclusive Pension Plan Design for a Diverse and Decentralized Workforce

By combining inclusive pension plan design with targeted engagement strategies, FAB organizations can close the retirement readiness gap and build long-term resilience for all employees.

-

Article 8 mins

Strengthening Workforce Resilience in a Changing Climate

Extreme weather poses growing risks to business operations and workforce resilience. Employers must go beyond reactive measures to protect employees and proactively plan for more frequent and widespread extreme events.

-

Article 13 mins

Cyber 2026: Evolving Threats Demand Strategic Leadership

In 2026, AI-driven threats and regulatory pressures make cyber risk a board-level priority. Now is the time for leaders to act decisively — strengthening resilience and leveraging a favorable insurance market.

-

Article 10 mins

Data in Supply Chains: Turning Insights into Action

Organizations have access to more supply chain risk data than ever — yet few use it to its potential. Leaders who turn the wealth of available information into actionable insight set the standard for effective, data-driven supply chain risk management.

-

Article 6 mins

From Threats to Tools: Evolving Risk Functions in Financial Institutions

The risk management playbook is being rewritten as financial institutions navigate an era of heightened complexity and rapid change.

-

Article 28 mins

2026 Human Capital Outlook: 5 Forces to Act on

As workforce expectations rise and business risks intensify, HR leaders must act on five forces shaping 2026 — from AI and skills to healthcare costs, analytics, pay transparency and retirement readiness. Discover how to build a strategy that balances performance, cost and experience.

-

Article 10 mins

From Compliance to Competitiveness: Sustainability for Finance Leaders

Sustainability is no longer reputational. It’s a strategic priority within risk and capital management, powered by robust data, innovation and industry expertise. For finance leaders, embedding sustainability into decision making can be critical to secure long-term value and earn stakeholder trust.

-

Article 12 mins

Workforce-Focused Analysis on GLP-1s: Phase Two Findings

Explore second-phase GLP-1 study insights on improved medical cost growth, adherence and women’s health.

-

Article 15 mins

Nuclear Energy Revival: Risk, Resilience and the Talent Revolution

Nuclear is a critical pillar of the energy transition, addressing the dual challenges of decarbonization and surging demand. Success will hinge on managing risks across new generation technologies, regulatory shifts, financial model changes, supply chain challenges — and the acute war for talent.

-

Article 9 mins

From Volatility to Value: Multi-Year Casualty Insurance and Structured Risk Solutions

In today’s volatile casualty market, businesses face mounting uncertainty from rising loss exposures and shifting risk transfer dynamics. Multi-year structured programs and other alternative risk transfer solutions can offer a smarter way to align risk duration with capital strategies.

-

Article 11 mins

The Digital Claims Transformation: What Risk Leaders Need to Know

As digital claims transformation accelerates, organizations are adopting AI, automation and analytics to improve speed, transparency and accuracy — and unlock deeper insights into risk profiles, enhancing long-term resilience.

-

Article 3 mins

U.S. Pension Risk Transfer (PRT): Annual Report Preview

U.S. pension risk transfer activity strengthened in late 2025, supported by competitive pricing and growing interest in buy-ins.

-

Article 6 mins

A Streamlined Retirement Solution for Spin-Off Organizations

Pooled employer plans (PEPs) can offer a streamlined solution to the retirement planning challenges inherent in spin-off and M&A events.

-

Article 4 mins

5 Myths You Need to Stop Believing About Litigation (and 7 Ways to Avoid It)

Litigation from workers’ compensation and liability claims is not inevitable. Discover common myths and seven practical strategies using prevention, documentation, and AI to help avoid lawsuits and protect your organization.

-

Article 7 mins

Credit Insurance and The Future of Energy

In a conversation with Trade Finance Global’s Deputy Editor, Mahika Ravi Shankar, Madeleine Whiteley, Senior Client Manager at Aon, explored how credit insurance is helping energy clients navigate volatility, adapt to the transition to renewables, and manage the uncertainties of today’s market.

-

Article 12 mins

Life Sciences at the Crossroads: Innovation, Access and Rising Healthcare Costs

Innovation has always driven growth in life sciences. Yet today, it’s not enough to keep organizations relevant and resilient. As global healthcare changes rapidly, the future of care depends on how well leaders align their breakthroughs with real-world healthcare delivery, affordability and trust.

-

Article 9 mins

As Health Spend Soars, Employers Should Beware of Hidden Cost Threats

While cancer care and specialty medicines are familiar culprits behind rising U.S. healthcare costs, benefit leaders should also watch out for less obvious factors driving up expenses. Taking a holistic view requires being aware of these hidden threats as you work to manage costs.

-

Article 8 mins

Optimizing Your Property Program: 3 Ways Analytics Can Deliver Better Outcomes

Advanced analytics empower forward-thinking risk leaders to secure better terms, anticipate volatility and build resilience. Explore three strategies to future-proof your property program through analytics.

-

Article 7 mins

Trump Administration Prescription Drug Initiatives: What Employers Should Know

The Trump Administration has introduced several initiatives aimed at reducing prescription drug costs. Here’s what these changes could mean for employer-sponsored plans.

-

Article 8 mins

Risk Factors and Conditions Driving the Global Medical Trend Rate

The global medical trend rate is projected to dip below double digits for the first time in three years to 9.8%. It may be a hopeful sign that cost increases have plateaued, but cost increases are still elevated. We explain the risks and conditions behind the increase so employers can prepare.

-

Article 9 mins

6 Insights to Build Risk Resilience in a Volatile Retail Market

Retailers in North America are navigating intense competition, shifting consumer demands and rising costs. Add to that a wave of evolving risks — from cyber to litigation — and the pressure mounts. These six insights can help retailers rethink their risk strategy.

-

Article 8 mins

Cyber Risk is the Weak Link in Data Center Construction

Data center construction is booming — but cyber risk management hasn’t kept pace. As digital infrastructure becomes ever more critical, fit-for-purpose insurance solutions are essential to protect projects from costly cyber events that derail timelines and budgets.

-

Article 7 mins

Captives and Cyber: From Tactical Response to Strategic Risk Optimization

Captives are moving from a reactive stopgap to a core, strategic tool for managing cyber risk — helping organizations drive efficiency, manage volatility and build resilience in a rapidly evolving risk environment.

-

Article 23 mins

Q3 2025: Global Insurance Market Overview

Buyer-friendly conditions persisted in Q3, with ample capacity and intense competition driving continued price reductions and broader coverage for preferred risks, especially in property, cyber, and directors and officers.

-

Article 10 mins

Resilient Infrastructure: 3 Risks to Watch

Cost inflation, project complexity and tight schedules aren’t the only pressures facing infrastructure stakeholders. Emerging risks — from design and contract misalignment to tech-driven vulnerabilities — demand proactive risk management across the entire project lifecycle.

-

Article 9 mins

Breaking the Silence – Tailored Strategies for Men’s Mental and Financial Health

Conversations at work about mental health and finances can be daunting. That’s especially true for male employees, who fear the associated stigma. Employers can help those conversations by supporting a healthy culture and providing benefits designed to help with financial and mental wellbeing.

-

Article 41 mins

Country-Level Findings

Explore how risk perceptions vary across countries with insights from Aon’s 2025 Global Risk Management Survey.

-

Article 5 mins

Rethinking Talent Strategy as H1B Visa Costs Rise

As H1B visa costs surge, organizations face complex decisions in talent strategy and global workforce planning. This article explores how employers, talent, and industry must adapt holistically to remain resilient and competitive amid sweeping immigration and market changes.

-

Article 10 mins

Latin America’s Risk Landscape: Turning Complexity into Competitive Advantage

Latin American organizations face converging risks, but those who rethink resilience can unlock growth and gain a competitive edge.

-

Article 1 mins

Regional Results

Aon’s 2025 Global Risk Management Survey explores how organizations across four regions are responding to top risks—revealing both the challenges they face and the opportunities to build resilience in a fast-changing world.

-

Article 12 mins

Rethinking Resilience: Addressing Asia Pacific’s Top Risks

Asia Pacific’s risk landscape is shifting fast. Organizations that rethink resilience as a strategic differentiator will be best placed to navigate volatility and seize emerging opportunities.

-

Article 10 mins

Rethinking Resilience: Navigating North America’s Evolving Risk Landscape

North American organizations face intensifying risks across cyber, supply chain, reputation, and talent. Those who rethink resilience and risk management can turn uncertainty into a source of competitive advantage.

-

Article 10 mins

Turning Uncertainty into Opportunity: Managing Risk in the EMEA Region

In a region shaped by volatility and transformation, EMEA organizations are rethinking risk and resilience to unlock competitive advantage and navigate a rapidly evolving global landscape.

-

Article 10 mins

Where Cyber Meets Physical: Rethinking Risk in the AI Age

From drones that dodge surveillance to deepfakes that unlock doors, AI is reshaping physical security. It’s time for risk managers to rethink how they protect their organizations.

-

Article 7 mins

Optimizing and Personalizing Benefits with Artificial Intelligence

There are a few important ways AI is already influencing the health and benefit ecosystem in the U.S. Here’s how HR teams can harness their vendor ecosystem and use this technology to influence better health outcomes for their workforces.

-

Article 13 mins

Securing Power: Global Strategies for Data Center Energy Resilience

Artificial intelligence is driving unprecedented demand for data center power, straining global grid capacity and reshaping energy strategies. Developers are racing to secure reliable energy but face complex risks and challenges.

-

Article 11 mins

High Stakes in High Tech: Securing the Technology Supply Chain

As in-demand, high-value technology cargo travels through complex supply chains, any disruption can trigger costly delays and reputational damage. Leaders can manage volatility with a future-ready risk management approach backed by innovative insurance solutions and data-driven logistics.

-

Article 5 mins

2026 Salary Increase Planning Tips

Global voluntary turnover remains low, shaping cautious 2026 salary budgets and prompting a renewed focus on employee development to sustain engagement. Employers are balancing cost control with strategic investments in skills, paying high performers, pay equity and total rewards.

-

Article 8 mins

Adapting to Disruption: How Financial Institutions are Reframing Risk

Financial institutions are navigating a landscape of converging risks, from cyber threats and regulatory complexity to economic volatility and geopolitical disruption.

-

Article 9 mins

Building Resilience to Support Growth in Construction and Real Estate

Construction and real estate organizations are navigating a risk landscape shaped by economic volatility, digital acceleration and workforce disruption.

-

Article 1 mins

Industry Insights: Findings from Aon's Global Risk Management Survey

Business risks impact industries in different ways. Aon’s 2025 Global Risk Management Survey reveals how organizations across nine sectors are responding to today’s most pressing threats—from geopolitical volatility and cyber risk to supply chain disruption and talent shortages.

-

Article 10 mins

Managing Risk and Unlocking Opportunity in the Food, Agribusiness and Beverage Industry

Surging input costs, supply chain fragility and geopolitical instability are reshaping the risk landscape for the food, agribusiness and beverage (FAB) industry. As organizations face mounting pressure on margins and operations, leaders are rethinking risk strategies to unlock resilience and growth.

-

Article 11 mins

Navigating Risk in Insurance: Turning Complexity into Competitive Advantage

Aon’s Global Risk Management Survey shows insurers face a convergence of risks — cyber, climate and geopolitical volatility — that demand strategic resilience, sharper underwriting and innovation to stay relevant in a shifting landscape.

-

Article 10 mins

Navigating Risk in Life Sciences: Building Resilience to Support Growth

Faced with fragile supply chains, regulatory upheaval and rising competition, life sciences firms are reframing risk as a strategic enabler – using analytics and alternative capital to protect innovation and unlock growth.

-

Article 10 mins

Navigating Risk in Transportation and Logistics: Gearing Up for Big Transitions

As geopolitical instability, workforce disruption and rapid technological change converge, the transportation and logistics industry is undergoing a strategic transformation. Organizations are rethinking supply chains, investing in automation and reshaping workforce strategies to build resilience.

-

Article 11 mins

Navigating Volatility in Natural Resources: Risk Management as a Value Driver

From business interruption and commodity price volatility to shifting regulations and cyber threats, risks are converging to reshape the operating environment for the natural resources industry.

-

Article 9 mins

Technology, Media and Communications: Rethinking Risk in a Shifting Landscape

As disruption accelerates across the TMC industry, organizations face a complex web of risks — from cyber threats and AI upheaval to regulatory shifts and intensifying competition. Leaders are rethinking risk to build resilience, unlock growth and stay ahead in a rapidly evolving landscape.

-

Article 10 mins

Turning Risk into Resilience in the Industrials and Manufacturing Industry

From commodity price volatility and economic uncertainty to supply chain disruption and cyber threats, the industrials and manufacturing industry faces a convergence of risks that are reshaping the operating environment and requiring a new approach to risk.

-

Article 6 mins

Optimizing Your Property Program: A Risk Capital Approach to Manage Volatility

Risk buyers can build resilience in their property portfolios by implementing a risk capital strategy that utilizes alternative risk transfer sources to access capital and support long-term program stability.

-

Article 10 mins

Cyber and E&O: Pricing Holds, but Market Momentum is Shifting

The global cyber and tech errors and omissions market continues to favor buyers — for now. As AI-driven threats, privacy litigation and supply chain exposures intensify, forward-thinking organizations are using this window to build resilience.

-

Article 10 mins

A Better Approach to Succession Planning Using Assessment Data

Succession planning is evolving. By gathering comprehensive data and adopting predictive approaches, organizations can better anticipate workforce needs and build deeper benches of future leaders.

-

Article 7 mins

Business Interruption: Managing Risk in an Interconnected World

Business interruption is the second-highest global risk in 2025 — but is expected to fall to seventh place by 2028. As interconnected threats multiply, from cyber attacks to climate events, organizations must diversify supply chains, embed geopolitical insight and regularly update continuity plans.

-

Article 6 mins

Cash Flow and Liquidity Risk: A Rising Challenge

Cash flow and liquidity risk re-enters the top ten global risks in 2025 — and is expected to remain in tenth place by 2028. Amid an uncertain macroeconomic outlook, organizations must strengthen forecasting and unlock working capital to build financial resilience.

-

Article 7 mins

Commodity Price Risk and Material Scarcity: An Escalating and Complex Risk

Commodity price risk ranks sixth globally in 2025 — and is forecast to climb to fourth place by 2028. With supply chains strained by geopolitical tensions and climate disruption, organizations should consider hedging strategies, diversifying sourcing and exploring innovative risk transfer solutions.

-

Article 6 mins

Cyber Risk: Turning Uncertainty into Opportunity

Cyber risk tops the global risk agenda in 2025 — and is forecast to retain the number one position through to 2028. As digital threats evolve, organizations should strengthen resilience, quantify exposure and adapt their risk strategy.

-

Article 5 mins

Damage to Reputation or Brand: A Critical Risk

Damage to reputation or brand ranks eighth globally in 2025 — but is expected to fall to nineteenth by 2028. In an era of cyber threats, ESG scrutiny and social media amplification, organizations should quantify reputational risk and embed preventive measures into enterprise strategy.

-

Article 6 mins

Geopolitical Volatility: Preparing for the Unpredictable

Geopolitical volatility ranks ninth globally in 2025 — and is forecast to rise to fifth by 2028. With conflict, trade disruption and political instability on the rise, organizations must monitor global developments, regularly assess operational exposure and conduct scenario planning.

-

Article 5 mins

Increasing Competition Is Intensifying Risk for Organizations

Increasing competition ranks as the fifth biggest global risk in 2025 — and is projected to climb to number three by 2028. As technological disruption, talent scarcity and geopolitical shifts intensify market pressure, organizations must embrace agility, and rethink competitive strategy.

-

Article 8 mins

Navigating Regulatory and Legislative Change

Regulatory change ranks as the fourth biggest global risk in 2025 — and is expected to fall to sixth place by 2028. As policy shifts accelerate across sustainability, technology, trade and the workforce, organizations must adopt agile compliance strategies and unlock proactive risk management.

-

Article 9 mins

Supply Chain or Distribution Failure: Navigating the New Normal

Supply chain failure ranks seventh globally in 2025 — and is projected to fall to twelfth place by 2028. As weather-related disruption, geopolitical tension and cyber threats converge, organizations must balance efficiency with resilience and diversify sourcing.

-

Article 1 mins

Top 10 Global Risks

As risks increasingly overlap and evolve, managing them demands more than reactive strategies. This chapter explores the top-ranked risks from the survey and highlights how organizations that take a proactive, integrated approach can turn complexity into opportunity.

-

Article 6 mins

Why Economic Slowdown is an Ongoing Risk for Organizations

Economic slowdown ranks as the number three global risk in 2025 — and is projected to rise to number two by 2028. Amid trade tensions, inflation and geopolitical instability, organizations must strengthen liquidity, enhance workforce agility and rethink capital strategies to stay resilient.

-

Article 11 mins

In Conversation with Iberdrola: Navigating Megatrends

Spanish energy multinational, Iberdrola – a leader in grids, storage and clean energy – talks with Aon about its efforts to adapt and respond to climate impacts through its shift towards renewables and building a workforce for the future.

-

Article 6 mins

5 Bold Predictions for the Future of Total Rewards

Total rewards professionals must adapt quickly to changes in the workforce. Whether it's personalization of benefits powered by AI or a whole new language around total rewards, the near future may look very different than the status quo.

-

Article 10 mins

Rethinking Pay for Performance in the Era of Pay Transparency

As pay transparency regulations increase, companies must update their pay-for-performance strategies and ensure performance management and compensation are clear, fair and well-documented.

-

Article 17 mins

5 Data-Driven Ways HR Can Optimize Costs

Data and analytics can unlock value for HR professionals in a variety of ways. From a unified global benefits perspective to personalizing total rewards, gathering and analyzing the right types of data help companies optimize what can be their biggest expense.

-

Article 12 mins

People Risks Are Rising: Here’s How U.S. Benefits Are Stepping Up