Introduction

The Total Portfolio Approach recently has gotten a lot of attention from institutional investors, yet it is often described in a way that is abstract and

doesn’t concretely represent the realities of how it is implemented. TPA means different things to different people, and there is a wide range of practices used by proponents of TPA. These “TPA practices” blend new approaches with rebranding of strategies that have been around for decades, many of which are widely used without being described as “TPA” by those doing them. Those looking to understand TPA must realize that it is not a well-defined approach.

It is an approach with a high level of delegation to the investment team to implement a highly active investment strategy, and there are many ways institutions implement that under the TPA umbrella.

Because TPA means so many different things to different people, it would be a disservice to say we either “like” or “dislike” TPA. Instead, it is more constructive to articulate which aspects of TPA we like and dislike, and for what kinds of institutions. In that sense, we will treat TPA like an a la carte menu where investors can pick and choose what they like.

What is the Total Portfolio Approach?

In our white paper “The Total Portfolio Approach: New Innovation or Rebranded Old Ideas?,” we wrote in detail about what TPA is—both the theory and practice—so we will only summarize it here. Proponents of TPA have said “TPA is not a monolithic methodology that can be applied off the shelf,” and further that “TPA is not a specific model with a singular destination, but rather a range of approaches.”1 Some have even said that “TPA is not a strategy, but a mindset—centered on preparedness rather than rigid planning.”2 As a result, it is not possible to describe TPA with exact precision.

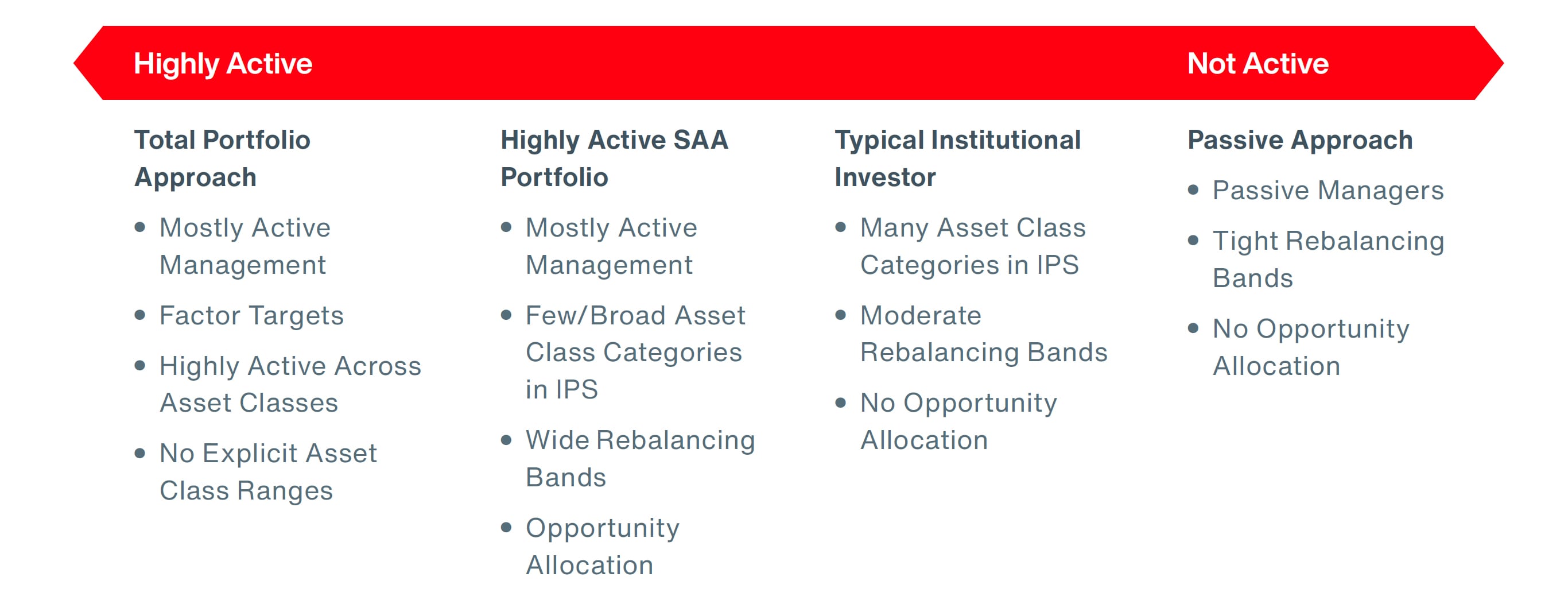

TPA is an umbrella term for a range of approaches to asset allocation and portfolio construction that are less constrained than traditional Strategic Asset Allocation used by institutional investors, and TPA typically involves giving an unusually high degree of discretion to the investment team to make decisions about implementation. We view it as the most active end of the spectrum of approaches to active management, as shown in the following exhibit.