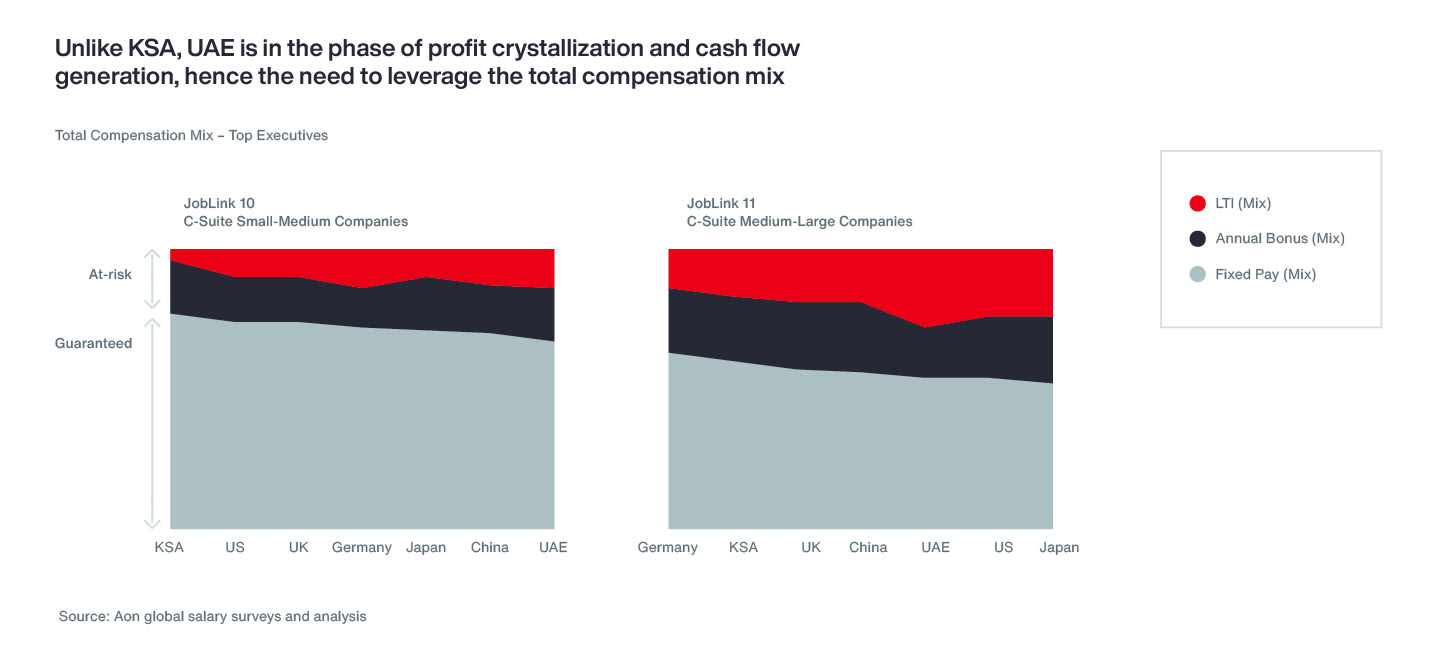

- The proportion of variable pay in executive compensation in Saudi Arabia (KSA) is lower compared to other developed economies. Increasing the proportion of pay tied to long-term incentive plans can help retain critical talent and align with long-term performance measures. Saudi-based real estate organizations can optimize the pay-productivity relationship by aligning more executive pay to be variable based on company performance through sales incentive plans, short-term incentive plans, and long-term incentive plans.

Competing for Talent – KSA and UAE

KSA has become the UAE’s main competitor in the war for talent. Real estate companies in KSA and UAE are at different stages of the real estate life cycle, with companies in KSA and UAE differing in their focus, operating models, structures and priorities. The market in UAE is focused on cash flow generation (i.e., sales) after years of intense real estate development whereas the KSA is focused on infrastructure development and construction.

Based on this, our hypothesis is that Saudi-based real estate organizations are focusing their attention on the UAE market for attracting critical talent in the development, delivery, construction and project management functions.

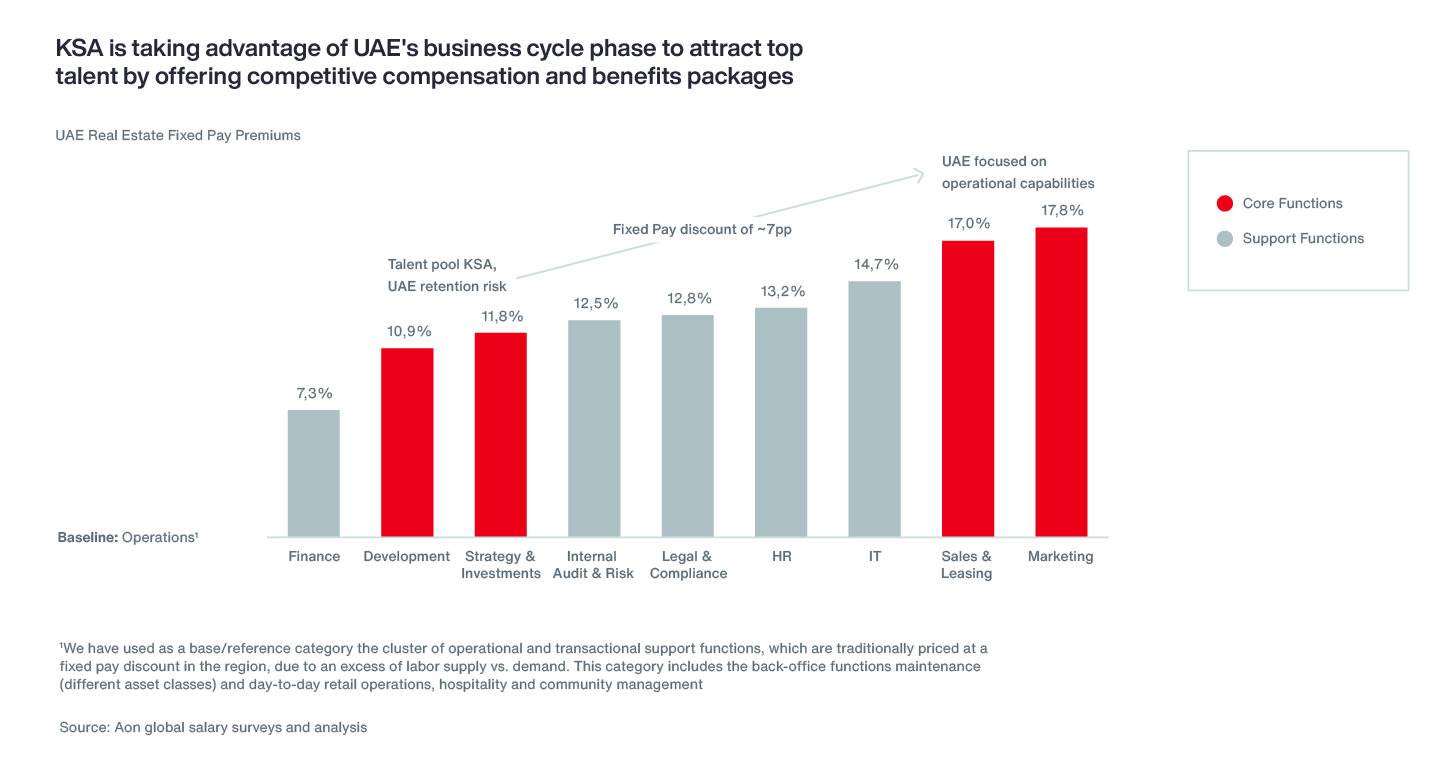

To test this hypothesis, we carried out a pay differential analysis for the UAE real estate sector market:

- Sales & Leasing, Marketing – The focus for players in the UAE is around bringing to market the stock of real estate (commercial, residential, and hospitality) developed over the past decade. This is reflected in higher salary premiums in Sales & Leasing and Marketing over other functions.

- Development, Strategy & Investments – These functions are paid at an approximate 7 percent discount to Sales & Marketing (after controlling for the impact of other pay drivers). It creates a flight risk for professionals working in these job families in the UAE, as they can take on more lucrative opportunities in Saudi Arabia with higher salaries. There have been instances of entire development teams in large UAE firms leaving to join large giga and mega development projects in KSA.

In response, companies in the UAE must rethink their compensation strategies and consider other measures such as career development, a positive work culture, and employee recognition programs if they are to retain their competitive advantage.

Navigating Talent Challenges

In a dynamic and competitive environment, real estate companies across the region must respond rapidly to market changes. They must stay current with key human capital trends and be prepared to navigate them. Rethinking human capital strategy is the key to success.

At Aon, we help companies across the real estate sector to make better human capital decisions, helping them to drive the change they need and maximize their investment in people. To get in touch with a member of our team to discuss the steps you can take, please write to [email protected].